Earnings per share (EPS) is a critical element of share valuation. Most investors use a modified approach to EPS by measuring it with respect to the CMP of the scrip (P/E ratio). EPS and P/E together account for an estimation of the "TIME required" for the stock to reach the current market price of the stock.

E.g. SCI (Shipping Corporation of India) is valued at 151 rupees a share and has an EPS of 50 rupees. In time, the total earnings over the next 3 years should be equal to 150 rupees (ceterus paribus). In such a situation, examining the EPS is crucial. This has to be looked at in the light of the change in pricing of products of the company (a lowering of price without a corresponding decrease in cost will decrease profits and hence value added to the company books), change in competitive scenario, change in management, change in strategy etc.

Look at change in strategy. State Bank of India has realised the pressures of competition and is looking at all products in a very professional way. Their foray into assets with differentitated products is amazing and so is the span of products they are providing. They are not challenging private banks, but are trying to rake in more market share from "other" nationalised banks like Central Bank of India, Indian Overseas Bank, Bank of India etc.

Now lets examine the Grahamian prophecy of "not" evaluating the earnings per share. Graham feels that predicting the earings of the company i svery difficult and not prudent as it is guided by the whims and fancies of the management. Graham lived in a time when corporate governance was a nothing and majority owners used to treat companies as proprietorships, whose assets and resources could be used for one's own advantage. Graham didn't believe that people are honest enough to allow enough profits for disbursements to public (or people were more dishonest than honest. Remember the blog on "Conservatism and Suspicions"). Understand that Graham also lived through a major depression.

E.g. GTL Limited has 72 rupees in cash and is availbale at 107 rupees. Now that's intrinsic value. The EPS of GTL is however very very low.

A strong EPS was a bonus for Graham but a strong NCA was the clincher.

I personally have a stronger allegiance to NCA rather than EPS as the cushion provided by value intrinsic in a company is higher than that in the days to come. As they say, "a bird in hand is better than two in the bush"

Tuesday, November 14, 2006

Why look and not look at EPS?

Bookmark this post: |

|

Tuesday, August 15, 2006

Buying a company - math of a problem

Three companies are up for grabs but you have money to buy two only. The management has given instructions for you to only consider companies which give a high "Return on Capital Employed" ratio. All three companies are equally priced. Here are the specs -

1. Company A earns a profit of Rs. 80 from a capital employed of Rs. 100

2. Company B earns Rs. 20 from a capital emp of Rs. 100

3. Company C earns Re. 1 from a capital emp of Rs. 20

Thus company A has an ROCE of 80%, company B has an ROCE of 20% while company C has an ROCE of only 5%.

You might be tempted to buy companies A and B as they definitely have a much higher ROCE as compared to company C. Lets do some further math here -

Case 1: You drop A and pick B, C

Your total profit would be 21 (20+1) while your cumulative cap. emp. will total 120 (100+20) .. giving you a total ROCE of 21/120 = 17.5%

Case 2: You drop B and pick A, C

Now your cumulative ROCE jumps up to 67.5% (81/120)

Case 3: You drop C and pick B, A

A total profit of 100 (80+20) and total CE of 200 (100+100) means, a combined ROCE of 50%

So while dropping company C may seem a good choice, it'll not be too appreciated by your management.

Implications - Such situations also come to light in corporate quarters. E.g. an increase in homeloan rates may lead to lowered demand for housing and hence the share price of banks would come down. The larger part of the puzzle is "what is the contribution of home loans to the bank's total asset disbursements". In a previous blog I had explained the same situation w.r.t. HLL and it's price war with P&G on the detergents front.

Bookmark this post: |

|

Wednesday, May 31, 2006

More ... sasta stocks

My picks for tomorrow will be :

1. Rane Engine Valve - small cap; should give quick money .. 15-16% in a week; stop loss at 320

2. Wockhardt - good stock at low price

3. Monsanto - At a PE of 13 and an expected PAT of almost 100 crs ... easy buy

4. Apollo Tyres - quick money; stop loss at 220

5. Balaji Telefims - Good NCAV; good PE for entertainment/media stock

6. Abbott India - sasta

7. NIIT Technologies - sasta; buy and hold

8. Fag Bearing - quick money stock

9. Rain Calcining

10. Madras Aluminium Co.

11. India Glycol - has upside; a PE of 7.02

12. Apar Industries - Excellent sales growth; long-term prospect

13. Aegis Logistics - Great sales growth; good traction; quick money

14. Gujarat Ambuja Export - brilliant PE though sales are slow

15. NOCIL - excellent turnaround story

16. Tinplate Co. of India - Amazing valuations

17. Ind Swift Labs - One of the cheaper pharma scrips

18. Ahmednagar Forging - Forget the zero dividend; has a debt-reap of 64% of m-cap

19. Andhra Pradesh Paper Mills - Amazing valuations

20. Jupiter Biosciences - Future growth story

Bookmark this post: |

|

Wednesday, May 24, 2006

Sasta stocks

This is all I've been listening and reading over the last two days. A friend at office tried an experiment on this - he picked ten random stocks given in the tabloids as ridiculously cheap stocks ... surprise !!! ... that herd of "cheap" stocks actually knoocked off 3.4% of an investors wealth in the last two days.

What did I do? I too bought some stocks on 22-May (when the mkt went down by 1000 pts). As I had only 80000 bucks, I divided the money among some 9-10 stocks. Here are my value picks -

a) Amtek India - I bought this again ... at 108 rupees. It's at 120 today.

b) Bank of Baroda - Bought at 227 rupees ... up to 239 rupees

c) Kalpatru Power - Amazing returns ... bought at 641 .... now up to 755 rupees

d) Mastek - up from my buy price of 307 .. up to 326 rupees

e) Rolta India - Bought at 184 rupees. Now at 194 rupees

f) Gujarat NRE - Bought a little more ... at 65 rupees ... its up to 75

g) Rain Calcining - 38 rupees .. 39.10 rupees

h) Tinplate Co of India - 73 rupees goes up to 77 rupees

i) Alembic - 328 rupees .. disappointing up to only 332 rupees

j) Alok Textiles - bought at 73.5 rupees ... at 77.15 rupees

I had my share of fun today .. the BSE fell by 250 points today ... and my portfolio actually went up a miserly 0.4%

Bookmark this post: |

|

Tuesday, May 2, 2006

The big bank theory

Bankex moved up by 4.02% today. That's huge. The major gainers were BoI, BoB, Andhra Bank, Indus Ind Bank, ICICI Bank Limited, Vijaya Bank and UTI Bank (all over 5% gains and all in BSE A segment)

Of all these, I like Bank of Baroda. At a fwdPE of 8.36, BoB is undervalued. I estimate a 1yr earning forecast of 800 crs+ given the legacy and advancements made by the bank. The current dividend yield is 2.20%, which is slated to increase given the rise in profits.

Bookmark this post: |

|

Sunday, April 30, 2006

Mutual funds and stock valuation

Its often a good idea to see what mutual funds are buying or selling these days. This helps you predict stocks which have a higher propensity of taking the dive or perhaps, soar the skies. I used MutualFundsIndia to list the top 4 performing funds over the last 3 months .. here's their list -

1. Deutsche Alpha Equity Fund - 37.35% in last 3 months

2. Sundaram Select Mid-cap Fund - 33.10% in last 3 months

3. SBI Magnum Comma Fund - 32.90% in last 3 months

4. Franklin India Opportunity Fund - 32.10% in last 3 months

Now, I guessed that the portfolio composition of all these 4 funds would tend towards parity or perhaps, a high correlation. If not companies, atleast the sectors. Here news -

1. Deutsche Alpha - Diversified (29%); Computers (9%); Metals (8%) ... top 3 cos: Sterlite (8%); Tata Steel (8%); Tata Chemicals (7%)

2. Sundaram Midcap - Engineering goods (17%); Housing (11%); Auto & ancillaries (11%) ... top 3 cos.: Kalpataru (4%); Balrampur Chini (4%); Ansal (3%)

3. SBI Magnum - Cement (14%); Diversified (13%); Metals (12%) ... top 3 cos: Hindustan Zinc (8%); Shree Cement (7%); United Phos (5%)

4. Franklin - Entertainment (22%); Auto & ancillaries (14%); Diversified (11%) ... top 3 cos: TVS Motors (9%); Jaiprakash (7%); Calcutta Electric Supply Co. (7%)

Amazingly ...

i) The top three sectors among the four top performing funds is strewn over 8 different industries (from a max:12)

ii) The top 3 holdings of each of the 4 funds is different i.e. we have 12 different companies that form the top 3 holdings of these 4 funds.

iii) The average holding in equities from the total corpus is a healthy 94%. (so you might want to rethink your idea of staying 60% in cash and rest in equity)

Mutual funds donot think alike and have different priorities and basis of evaluating stocks. For us the advantage is in identifying changes in portfolio in mutual funds to understand what they are buying or selling, researching the same and arriving at a decision.

PS: Has anyone checked the Calcutta Electric ... ???

Bookmark this post: |

|

Nahar Industrial Enterprises Limited

Nahar Industrial Enterprises Ltd. The company results have been very impressive over the last 3 quarters -

Jun-05: Sales increased to 176 crs from 90 crs LY; profits up from 3 crs to 14 crs

Sep-05: Sales up from 82 crs to 172 crs; profits rose from 7.12 to 15.07 crs

Dec-05: Sales upto 169 crs (from 156 crs); profits up from -0.72 to 18.26 crs.

Extrapolating these numbers over the next 3 quarters puts the fwdPE of the company at a powerful 8.56. I also find that -

1. The organisation's interest cost has been decreasing over the last few quarters, which is brillant. (there is one news item however, which indicates that the company is in discussion for issue of FCCBs)

2. The NCAV of the scrip is 13.92 with a sizable investment head of 66 crs in the balance sheet (mostly owing to shares in sister concerns - NSML and NEL)

3. A visible increase in net margin from -1.5% in FY2004, 3.3% in FY2005 and 9.2% till Dec-05

4. Surprisingly, no dividend has yet been issued although the company has enough cash reserves and cash profits.

5. The 31-Mar-05 book value is a comfortable 175 rupees/share

I would love to buy this stock. The only hitch on the charting is : the scrip had just created a valley a few days back when it dipped from 170 rupees to 130 rupees. It's now back to 170 rupees. Dont risk market timing ... buy a small number of shares, buy more on declines.

Bookmark this post: |

|

Saturday, April 29, 2006

Alembic Pharma

Watch out for this stock. I advice BUY on declines in the price of the stock. Reasons -

1. Alembic has come out with a good Q4 result, displaying a strong increase in PAT (from 6.36 crs to 17.10). This is in line with earnings over the last few quarters.

2. The yr has closed at an EPS of 28.36. With the CMP at 401 (29-Apr), the PE comes to 14.13.

3. Sales have risen by 20% plus on every Q-on-Q results and so have profits. A lil' extrapolation would put Alembic's next 2 Qs results at a strong footing equaling around 16 rupees in EPS. I would picture Alembic at a fwdPE of 12.9 which is one of the lowest in the Indian pharma space.

4. The heavier part of the sales growth has come from domestic sales (around 77%) however interestingly, Q4 has contributed one-third of the entire export pie. This marginally indicates a move towards ramping export operations by the company.

A 99 yr old company, stable sales and profits, growing, a relative inexpensive valuation to peers ... worth a buy.

Bookmark this post: |

|

Wednesday, April 26, 2006

National Organic Chemical Industries Limited

or NOCIL for short. NOCIL is a turnaround story ... refered to BIFR in Jan-2004, it came out of bankruptcy with a positive net worth on 31st March 2005. The company had a fantastic 3rd quarter with an impressive 23 crs of profits on a capital base of 160.79 crs. Over the last 9 months, the company has notched up 59.50 crs of profits and should close at around 80 crs for the yr. The fwdPE of the stock would be a comfortable 5.63 - an alice in wonderland situation !!!

And although the company doesn't provide for any dividend, I take comfort over the fact that NOCIL has an NCAV of 4.07 and a book value of 10.90 (as compared to a CMP of 28.25). The high court has approved of a demerger of the company in two divisions to which the shareholders will benefit as the rubber division will take advantage of an independent management.

Peers of NOCIL would be other petrochemical companies like Castrol, Manali Petro, Narama Chematur, Hind Flourocarbons, Sah Petroleum, SA Petrochem, Lanxess ABS, Chemplast Sanma, Jubilant Org, DCW, IPCL and Finolex ... (barring Sah whose profits are almost non-consequential, NOCIL and Narmada Chematur exhibit the best improvements in qtrly earnings ... Narmada Chematur has also been recommended for a buy in a previous blog).

I would place a BUY on NOCIL with a stop loss on 24 rupees.

Bookmark this post: |

|

Nahar Export revisited

Nahar Exports Ltd has informed BSE that ....

Thus upon sanction of the scheme shareholders of the Company holding 100 Fully paid up equity shares of Rs 10/- each on the record to be fixed for the purpose, shall receive 55 Fully paid up equity shares of Rs 5/- each in NSML (post demerger of investment business) and 70 Fully paid equity shares of Rs 5/- each in the Company.

Questions -

1. Any arbitrage?

2. short/mid/long term prospects?

There was one report by EmKay which talks of latent (and now exposed) shareholder value in this deal. Here's how ...

1. The invt business in NSML (Nahar Spinning Mills Ltd.) is worth 346 crs which'll be merged with NCFSL (Nahar Capital and Finance Services Ltd.). Allotment ratio: 1 equity share of NSML = 1 equity share of NCFSL (FV Rs 5) + 1 equity share of NSML (FV Rs 5)

2. Textile business of NEL (Nahar Export Ltd) to be hived off and merged with NSML. Allotment ratio: 100 shares of NEL (FV Rs 10) = 55 shares in NSML (FV Rs 5) + 70 shares NEL (FV Rs 5)

The investment summary presented : a sum-of-its-part valuation of NEL gives Rs. 112 as the fair value of the stock. Hence the potential upside of NEL is 38%. (for a copy of the report, kindly email me)

Bookmark this post: |

|

Sunday, April 23, 2006

Paper

Surprisingly, the paper industry has been an underperformer. It's PE ratio has often been between 5 and 10, which is mighty lower than most other core industries. .. but things are looking better for this industry (story). An 8% growth in GDP means an 8% plausible increase in demand for paper, while the production is expected to grow at only 4%. This would lead to a rise in prices and hence profitability. Also, there will be consolidation in the industry with the smaller players merging with bigger ones (primarily due to the introduction of environmental norms). Players are also getting ready to explore the export market with 10-12% of the produce leaving Indian shores. (This would fuel prices even further)

Lets examine the prospects of a few players -

[1] West Coast Paper Mills Ltd. - The lastest quarterly data pegs the company at 537 crs of sales and 42 crs of profits. At a CMP of 393 (21-Apr), the PE is at 8.37. The company has also indicated an improvement in the net margin owing to cost control measures (and inspite the increase in fuel costs). It's a BUY candidate.

[2] Andhra Pradesh Paper Mills - I bought this a week back at 120 rupees. It's at 140 rupees today (21-Apr). The scrip has a fwdPE of 10.11. A recent report by EmKay Research gives the following cues -

a) Margin will double from 13.5% to 26.2% in the next two years

b) A 125% improvement in PAT over the next two years. In fact at today's price, the research agency estimates the stock to reach a PE of 4.4 by FY2008

c) Sales growth at a CAGR of 15.20%

d) The price target for Andhra Paper Mills is INR 224.00 (an increase of 76% from current levels)

[3] JK Paper - Here's another research report by Religare Securities Ltd. The CMP of JK Paper is 60 and it has a price target of 96 rupees. I'd however, prefer Andhra Paper Mills and West Coast over JK Paper as the company has shown a lack of consistency in profitability (profits went down by 8% last yr and sales were stagnant)

[4] Star Paper - Here's a pick of the week by icicidirect.com. Star Paper Mills has perhaps the lowest PE valuation in the paper industry ... a fwd PE of just 6.20. The company has shown brillaint improvement in sales with one glitch in the quarter ending Dec-05, where PAT was only 2.40 crs ... a huge reduction over last yr. So any investment in the scrip can be recommended only after checking the Mar-06 results of the company.

So here it is ... divide you paper industry booty equally between West Coast Paper and Andhra Paper Mills. They are a t good valuations, have grwoing sales+profits and good management structures.

Bookmark this post: |

|

Saturday, April 22, 2006

God knows why but my broker friend is extremely bullish on ...

In a recent post, Amit had penned the following comment :

Hello shankar,

My broker is extremely bullish on jHUNJHUNWALA VANASPATI.This stock has been hitting circuits for the past some time,the current market price(at todays circuit) is 58.He expects it to reach a three figure mark in a months time(atmost).

One other stock is UB enginerring trading at 63(todays circuit) which has also hit circuits almost daily in the past few days....

Will look forward for your advice on UB Engineering and JHUNJHUNWALA VANASPATI.

God knows what but my broker friend is extremly extremly bullish on JHUNJHUNWALA VANASPATI.

Best regards,

Amit.

Jhunjhunwala Vanaspati has risen from 40 rupees (Mar-28) to 65 rupees (Apr-21) - a return of 62.5% in 3 weeks [Charting]

On a more sanely and boring front, lets examine the financials of this scrip -

1. The stock is at a fwdPE of 6.12

2. Has been profitable over the last 5 yrs and all quarters are in the black (this isn't some small company .. it has sales of almost 500 crs)

3. Although quarterly profits are not high .. the company should close the yr with 10 crs of PAT

I would advice a small sum of money (not to be entirely taken as a gamble) ... towards this company. Keep a stop loss of 50 rupees however.

UB Engineering was at 32.95 (Mar-28) and has risen to 66.00 rupees (Apr-21) without a single day of negative returns .. one reason why Amit has not been able to lay his money on this stock [Charting]

UB Engineering has been posting losses for the last 4 yrs. One reason for recommending this stock can be the expectation that UB Engineering will be in the black this quarter like the previous one and perhaps actually, have had made some money. I would advice a "no buy" on this scrip.

Bookmark this post: |

|

Abhishek Industries

The Trident Group came as a shocker for the PGPM 2000-2002 batch of MDI, Gurgaon. The year was perhaps the worst, in salaries given to B-school students. Companies, on the other hand, were having a wonderful time picking students at dirt cheap packages. (I started at a take home of 19k p.m. which incidently, was higher than batch median ... whatever the tabloid might have said). Trident entered the campus as a Day 3 company and offered a package of 38,000 rupees p.m. .... a package that even batch toppers were deprived of.

The financials of Abhishek Industries :

1. The sales and profits have grown at 25% over LY and the Q-on-Q numbers have been impressive

2. I expect a closing of 51 crs for this yr ... an EPS of 2.62 rupees/share and a P/E of 11.35 which is much lower than competitors like Welspun India whose PE is at around 22.

3. A little high on debt, but has a good BV/share of 14.6 rupees

4. Two small hiccups .. Abhishek has not given a single dividend in the last five years and, has a negative NCAV (am not giving too high a priority to this however)

Abhishek Industries is a fantastic candidate for "buy and hold". The downside in the stock is minimal and has an excellent management team. The annual report (pdf, 6.20 MB) of the organisation calls for an excellent reading (dont miss the managements' discussions and analysis part .. pgs 46-57).

I would throw a buy on Abhishek Industries .. to be held for long.

Bookmark this post: |

|

Scrips I don't like

4 codes ... Buy / Wait / Pricey / Penny ... is what I use in my stock tracker.

Buy means an under-valued stock

Wait means a stock, fairly valued .. yet in contention if the price reduces

Pricey is a stock, over-valued and hence, not in contention yet

Penny is the scum-stock ... ones I'll stay away from for a long time

Here's a list of some I've classified as "Penny" (some changes may be done from this list on account of fundamental changes to the scrip) ... the primary reason for not investing in these stocks is the low profit levels exhibited by the below stocks

Silverline Technologies Ltd.

Tele Data Informatics Ltd.

Jindal Worldwide Ltd.

Shyam Telecom Ltd.

Vardhman Spinning and General Mills Ltd.

Saurashtra Cements Ltd.

Rain Commodities Ltd.

Morarjee Realties Ltd.

Selan Exploration Technology Ltd.

Prakash Industries Ltd.

Birla VXL Ltd.Mysore Cements Ltd.

Andhra Cements Ltd.

LML Ltd.

Moschip Semiconductor Technology Ltd.

Andrew Yule & Company Ltd.

IFCI Ltd.

Consolidated Finvest & Holdings Ltd.

FCGL Industries Ltd.

Sterling Holiday Resorts (I) Ltd.

Sharyans Resources Ltd.

Gujarat Sidhee Cement Ltd.

Swan Mills Ltd.

Premier Explosives Ltd.

Jay Shree Tea & Industries Ltd.

Ruby Mills Ltd.

Bhansali Engineering Polymers Ltd.

Mahindra Gesco Developers Ltd.

AVT Natural Products Ltd.

Suprajit Engineering Ltd.

J K Industries Ltd.

Agro Tech Foods Ltd.

Liberty Shoes Ltd.

Polyplex Corporation Ltd.

Sirpur Paper Mills Ltd.

Shriram Overseas Finance Ltd.

Gujarat Apollo Equipments Ltd.

Forbes Gokak Ltd.

Samkrg Pistons & Rings Ltd.

Himachal Futuristic Communications Ltd.

Empee Sugars and Chemicals Ltd.

Energy Development Company Ltd.

Aksh Optifibre Ltd.

ABG Heavy Industries Ltd.

UTV Software Communications Ltd.

Yokogawa India Ltd.Prime Securities Ltd.

Cyber Media (India) Ltd

Eimco Elecon (India) Ltd.

Harrisons Malayalam Ltd.

Kalyani Forge Ltd.

Venky''s (India) Ltd.

Revathi Equipment Ltd.

Standard Industries Ltd.

Sarla Polyester Ltd.

Themis Medicare Ltd.

Goodricke Group Ltd.

Ramco Systems Ltd.

Nesco Ltd.

Om Metals Ltd.

Z F Steering Gear (India) Ltd.

Texmaco Ltd.

Star Paper Mills Ltd.

Madhucon Projects Ltd.

Transgene Biotek Ltd.

Indian Hume Pipe Company Ltd.

Central India Polyesters Ltd.

Swaraj Mazda Ltd.

Anant Raj Industries Ltd.

Ondeo Nalco India Ltd.

Scooters India Ltd.

International Travel House Ltd.

State Trading Corporation Of India Ltd.

Megasoft Ltd.

Spel Semiconductor Ltd.

Saregama India Ltd.

Faze Three Ltd.

Eskay Kn''''''''IT (India) Ltd.

Kale Consultants Ltd.

Force Motors Ltd.

S B & T International Ltd.

Deepak Nitrate

Mather and Platt (India)

Excel Industries

Bharat Gears

Triton Valves

Liberty Phosphate

Advanced Micronics

Bookmark this post: |

|

Monday, April 17, 2006

Torrent Power SEC Limited

After living in Delhi - Ahmedabad and Surat came a great respite .. from power cuts. The AEC (Ahmedabad Electricity Company) and SEC (Surat Electricity Company) are governed by Torrent Power and both stocks have good valuations .... SEC being the better half.

1. SEC gives upwards of 10 crs every quarter and would close the year at 60 crs.

2. The stock is available at a fwdPE of 9.15 which is pretty good.

3. The energy sector is on an upscale and Surat's energy consumption is surely on the rise ... aren't you hearing news on textile and diamonds more often ... ?

One pt. - the growth of the company will be dependent on the geographical spread. So although I see an upside to the stock ... maybe hitting 720 rupees in the next 3-4 months ... further holding will need to be checked with every quarter.

Bookmark this post: |

|

Sunday, April 16, 2006

Hexaware Technologies

Hexaware is a global provider of IT and Process outsourcing services with presence in the Americas, Europe and the Asia Pacific region. The company has an active base of over 100 clients and has companies like Peoplesoft and SAP as partners. It operates in the HR outsourcing space. Net net, Hexaware is a new-age technology company ... and ... the valuation is very interesting. Measure this :

1. Revenues have grown by 24.3% over LY and is now at INR 678.6 crs (press release)

2. PAT grew at 43.6%; now at INR 91.4 crs

3. 39 new clients added; 129 active clients

4. At a CMP of 150 (Apr-15) and a share capital of 23.48 crs (FV per share is 2.00 rupees) ... the P/E comes to 19.13.

The company has given a guidance for Q1 FY2006: 167 crs in revenue and 23 crores in profits ... which spells the growth objective of the organisation. Extrapolating the expected growth in business (as a function of manpower recruited, clients added, previous trends), I find the company well on course to reach a 1000 crs of revenue by 2008. Thus, profits will also rise at a CAGR of 27%. I estimate the 1-yr fwdPE at 16.6 which is much lower than peers such at 3i and Matrix.

Hexaware Technologies is a long-term buy.

Bookmark this post: |

|

Saturday, April 15, 2006

AVP

Alien v/s Predator is a Hollywood flick where a team of archeologist discover an Aztec temple under the Antarctic circle, housing a host of alien creatures .. none better than the Alien family and that of the Predator lineage. Only one will win.

A similar comparison can be made in IT stocks .. the biggies .. esp. after the wonderful guidance given by Infosys Technologies Ltd. a couple of days back. I put four IT companies to the test - Infosys Technologies, Satyam Computers, TCS and Wipro. All the above companies have a m-cap of over INR 25,000 crores and have over INR 750 crores of LY profits. All carry virtually zero debt in their balance sheets, are cash-rich businesses and have strong management. And yet there are a number of differences which can be analysed and exploited -

1. Growth in profits has been rather different for all 4 companies. I find that TCS has shown the fastest growth in profits over LY at 42%, while Infosys has been the slowest with only 16% growth. (Satyam - 20%; Wipro - 31%)

2. CMP/NCAV would mean the "margin of safety" that Graham has so often cited in his many illustrations. The ideal number is 0.66. However this number is more true for old economy businesses and not for new sector business like IT services. For the record, Satyam is the best here with 8.66, while TCS has 37.79. (Wipro - 19.73; Infosys - 21.95; NCAV includes investments too)

3. At current prices, I estimate the fwdPE of all four companies at - Satyam - 27.91; Infosys - 37.38; Wipro - 37.81; TCS - 33.31

4. Cash per share - Satyam is at #1 with 75 rupees/share while Infosys is #2 with 54 rupees/share

5. While the dividend yeild of all 4 players is below 1%, Wipro is the best of the lot with a 0.96% dividend. Infosys however just pips Wipro with the special dividend of 30 rupees/share declared recently.

Examining these numbers, I feel Satyam is a good buy at the current price. There is an expectation of a bonus issue from Satyam aswell or a big dividend (it has crazy amounts of cash and is not eyeing any acquisitions).

PS: The movie was pathetic !!!!

Bookmark this post: |

|

Wednesday, April 12, 2006

Why panic?

The sensex fell 300 points on 12th April and another 100 points on 13th April ... and people are saying all kinds of things. Some important facts -

> the market has gone down by just 3.44% over the last two days. This is much better than those days when some of our stocks have gone down by 10% or more.

> a 400 pt drop reduces the current sensex P/E by almost hundred bps. So this should be at 19, right?

> corporate profits have improved over time ... nothing drastic has happened in terms of reduced exports, still higher fuel prices (it's remained the same over the last three quarters), global downturn. Infact exports have jumped, global economy is also on a high, real estate, gold prices and commodities are increasing .. things are getting better. Now an improvement in corporate earnings by 10%, would result in a reduction of PE by 180 bps. So your PE will go down to 17.20. If corp earnings is up 15%, then PE is 16.35.

It's my opinion, that the market will be upto 12000 by the end of May. Watch !!!!

Bookmark this post: |

|

Tuesday, April 11, 2006

Bloddy coincidence

I maintain a fairly extensive stock tracker which gives me a decent idea of NCAV, P/E ratio, fwd PE, debt recap numbers etc. Two stocks - Aarvee Denim and Exports Ltd. and Nahar Exports - are listed sequentially there. Surprisingly ...

1. Both stocks have an m-cap of 290 crs

2. Both stocks give a dividend of 1.50 on a 10 rupee share

3. Both stocks have similar debt recap value of 105 crs and consequently, the same ratio of debtrecap/m-cap

4. Both stocks have the same fwdP/E ratio of 7.90

I had put Nahar Exports on the BUY list a month back when it was at 70.00 rupees (the stock has jumped up to 89.00; I bought this stock yesterday at 82 .. so I made 9% in a day ... ha ). Im putting a buy on Aarvee Denim and Exports Ltd. aswell. The stock is available at 132 rupees (11-Apr), is largely profitable at 37 crs (expected this yr), growing sales and profits and good management.

Bookmark this post: |

|

Wi-fied Pune

A jolly good progressive plan in India " ... a 400 sq km area of Wi-Fi connectivity will enveloping Pune ... " surely raises many an eyebrow. But this seems a reality as the Pune Municipal Corporation and Intel have joined hands to do just that. Here's the link to the article in the Economic Times. Surprisingly, this project would cost the Pune Municipal Corporation a sum of only 7 crores, which means ... Wi-Fi is a truly inexpensive and a quicker option to cables connecting homes to broadband or dial-ups.

Which means ... better infrastructure in Pune, attractive IT destination ... higher property prices. Got that?

Bookmark this post: |

|

Monday, April 10, 2006

Su-Raj diamonds

Su-raj Diamonds should explode at the bourses. Some reasons -

a) The scrip is at a fwdPE of 7.55

b) The NCAV of the stock is a good 97.60 rupees while the CMP is much lower at 64.15 (Apr 7th) - a true Grahamian stock !!!

c) Cash rich company with 26.50 rupees of cash per share

d) Has a dividend yield of almost 2% (which is a rarity these days)

e) The company also has investments of 43.21 crs on it's books

The growth in sales has been good and consistent ... 495 crs (FY02), 583 crs (FY03), 723 crs (FY04) and 1028 crs (FY05). The company would close at 1150 crs for this financial yr ... another rising sales yr. Likewise, growth in profits is at 10.97 crs, 12.11 crs, 21.89 crs and 30.69 crs over the last 4 yrs. I estimate the profits for FY06 to close at 34 crs.

Note, that the P/E ratio of Su-raj Diamonds is much lower than it's peers - Vaibhav Gems, Goldiam International, Rajesh Exports, Shrenuj & Co. etc.

However, Su-raj Diamonds has never moved much. Movement has largely been between the 50 rupees to 70 rupees range over the last one yr. Surprisingly, a number of analysts have given a thums up to the stock over the short and medium term. Here's one by ICICIDirect.

Is this stock worth investing in?

Bookmark this post: |

|

The God of Pennies

I first tracked Hindustan Dorr-Oliver Ltd. in the summer of 2004, somewhere in the month of May. The stock was lingering at around 36 rupees per share. A lot has happened to the stock price and the company over the last 24 months. I am kinda shaken over the current price of the stock, especially when I measure it up with the profit numbers (quarterly data) of the stock ...

Mar-04: 8.78 crs; Jun-04: 0.04 crs; Sep-04: -0.38 crs; Dec-04: -0.91 crs

Mar-05: 2.37 crs; Jun-05: 0.37 crs; Sep-05: 0.39 crs; Dec-05: 2.90 crs

As on 7-Apr-2006, the CMP of the company is at 847.00 rupees. So here is a stock which is at a trailing PE of 154.20 and a fwdPE of 97.90; with an EPS (fwd) of around 9 rupees per share .. and yet commands a market value of 489.52 crores.

Take a bow, gentlemen ... you've just met the god of 'pennies' !!!!

Bookmark this post: |

|

Sunday, April 9, 2006

Munjal Auto

The consistency of growth in sales and profit numbers of Munjal Auto is truly remarkable. The sales / sales growth over LY and profit / profit growth over LY is listed below -

2002 : Sales - 105.63 crs (49.4%); Profit - 11.97 crs (148.0%)

2003 : Sales - 126.61 crs (19.8%); Profit - 13.15 crs (9.80%)

2004: Sales - 159.13 crs (25.68%); Profit - 19.68 crs (49.6%)

2005: Sales - 246.10 crs (54.65%); Profit - 25.98 crs (32.01%)

I estimate the FY2006 numbers on the sales and profit front to close at -

2006: Sales - 375.00 crs (52.37%); Profit - 34.00 crs (30.86%)

Some other important stats about the company -

a) The fwdPE of the scrip is 14.49, which though is not the lowest in it league .. is however among the better one. (I ran a massive filter on some 250+ auto ancillary companies for a minimum of 100 crs sales, profits of atleast 20 crs a year, qtr profits of atleast 6 crs ..... Munjal Auto came a #4 after Pricol, Subros and Amtek India ... I have put the entire list in the comments section)

b) At a dividend of rupees 4.00 for a 10 rupee share, the yield comes to only 1.63%. However, it is estimated that the payout for this yr would gross closer to 5.50 rupees.

c) The NCAV of the scrip is negative 11.52 due to the use of debt, which I feel is never a bad strategy as long as there is enough money to service the debt.

Although Munjal Auto's future is closely linked to that of it's more illustrious customer, Hero Honda Motors Ltd. and to the motorcycle industry per-se - I find the future of the company in good hands. At rupees 245.00, the stock may be a bit higher than the price I might want it at but I am comfortable in looking at a small investment and jacking up if the price diminishes in the short run.

Bookmark this post: |

|

Dial M for ... MRF

It's my opinion that MRF Tyres is overpriced. The scrip touched an all-time high of 3,895.00 rupees on 7th Apr. The charting of the company is enclosed .... (notice the price rise - extreme right)

- Notice the price stabilisation at the 2800-2900 levels (Oct-mid to Jan-end) and once again at the 3100-3200 levels (Feb to Mar). Net net, the price of the stock has vacillated between 2700 and 3250 over the last 7 months.

- The biggest movement post quarter result was when the scrip moved from 2800 to 3230 over 4 days.

- Suprisingly, the scrip has moved from 3050 to 3895 in 6 trading sessions : an increase of 27.7% ... with no supporting news.

- Q1 for the company was marginally better than Q4 of FY2005

At a CMP of 3895.00, MRF is at a fwdPE of 27.76, offers a dividend yield of 0.51%, has a NCAV of only 151.30. The input price (rubber) is on a rising trend - increasing by 50% over the last 12 months (the company is feeling the pinch of the same ... between March and July - historically, rubber prices tend to swell)

It's my opinion that the stock will be range bound ... 3500 to 4000. Which means, there is still money to be made by selling the stock short. An option will need to be considered, however. More on this, if I succeed.

PS: On April 3rd, MRF announced that it'll produce helicopter tyres once it gets the approval. Apparently, Brian Lara was in town for the launch of the same. Surely, that cant be the reason for the huge rise in the stock price.

Bookmark this post: |

|

Tuesday, April 4, 2006

Good advice

1. The recent bull run is a fantastic opportunity for you to sell-off stocks which have not given good profits (and in the future, have a greater probability of not giving you desired returns). So if you haven't done that yet, please use this to it's fullest.

2. Further investment in stocks should always be on the basis of good investment principles. Some ideas -

> Profit for the yr should be no less than 30 crs with a min of 6 crs per quarter

> Exhibit increased sales and profit growth over last three years

> Sales and profit growth for last 4 qtrs vis-a-vis LY quarters

> Price/BV less than 3

> P/E should be less than 66% of industry P/E (mostly fwdP/E < 12)

3. Always see the charting of the stock. www.bseindia.com and www.nseindia.com have the best charting features i've come across. Note, the support and resistance levels over the last one year.

4. Always have a stop loss for any stock you purchase. (and sell when the stop loss is breached; some Buffett-wanabes may think otherwise)

Bookmark this post: |

|

Sunday, April 2, 2006

GNFC Limited

Gujarat Narmada Valley Fertilizers Company Ltd. specs are enclosed -

Share Capital - 146.48 crs

Loans - 299.08 crs

Investment - 218.05 crs

Net CA - 292.47 crs

FV - 10 rupees per share

Dividend - 3.75 rupees per share

CMP - 115.00 rupees per share

LY Profits - 224.20 crs

Examining the balance sheet and the financial statements, I find -

1. The estimated profits for this year would be 270 crs which means a fwdPE of 6.24. Consequently, the sales have been growing at 12% over LY while profits are up, 30% over LY.

2. A dividend yield of 3.16% (on current levels) would only go up this year given the increase in profits. I estimate a dividend payout of 4.5 rupees per share which will propel the dividend yield to 4.11%

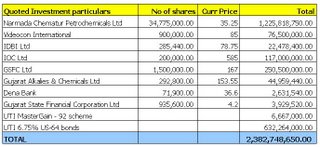

3. The investments shown in the books is at 218 crs. On going through the quoted investments in the balance sheet, I found that the current value of the quoted investments alone comes to 238.27 crs. These are liquid investments and hence can be included in the NCAV also. Here's a review of the quoted investments -

4. NCAV for the scrip (excl investments) is negative 0.05. By including liquid investments (and only 70% of it; I am keeping the remaining 30% as buffer for any plausible reduction in value), then NCAV comes to 14.43 rupees per share.

Finally, news value ... the big news for the company is the merger of the company with it's subsidary, Narmada Chematur Petrochemicals Ltd. The merger proposal was cleared on 2-Mar-2006.

On first count, it seems that this merger is not likely to disturb shareholder value of GNFC. Some reasons are enclosed -

1. NCPL is a profitable company with positive and growing profits QonQ.

2. Amazingly, the current dividend yield and the P/E ratio of this subsidary are better than GNFC (4.26%, 7.21)

3. A consolidated picture would thus be something like -

a) The GNFC share capital would increase by 20.54 crs to 167.02 crs

b) PAT for this year for the combined corporation would close at 300 crs. Thus the fwdPE would be 6.40.

It's a buy from my end with a stop loss at 100 rupees. But also look at NCPL ... seems to be some kind of arbitrage here ...

An arbitrage opportunity :

For every 3 NCPL share, one gets 1 GNFC share. Now GNFC is at 115 rupees and NCPL is at 35 rupees. Which means, if I purchase 3 shares of NCPL at 35 rupees each, my purchase cost would be 105 rupees. And when it gets converted to 1 share of GNFC, the same 105 would be worth 115 rupees. There are many a caveat to this ... but on the face of it, it's almost risk-free.

Bookmark this post: |

|

Micro Inks - a discussion

An interesting discussion on this stock is on at http://valueinvestorindia.blogspot.com. A few premises have been laid -

1. Is the German parent in attempt to delist the company?

2. Or, has something gone terribly wrong - with directors resigning and selling shares?

3. Significance of an open offer of 675 rupees/share to the shareholders of the company on Jan-13-2006. (the steep slide in the share price of the scrip started from then, when it came down from 625 rupees to 410 rupees in the next 30 days)

4. The analyst presentation is rather low on the business strategy of the company. Infact, more stress has been laid on how MHM Holding GmbH can exploit synergies by making India the production base for all it's subsidaries abroad.

... the company has an NCAV of 126 rupees per share which is excellent and a fwdPE of 16.52. Any insights?

Bookmark this post: |

|

The Adventures of Ponty Manesar

Amit has posted a hilarious compilation on the 'Adventures of Ponty Manesar' by Eldo Scaria. The links to the trilogy is enclosed :

1. The Adventures of Ponty Manesar

2. Further Adventures of Ponty Manesar

3. Even more Adventures of Ponty Manesar

The third ODI in Goa, between India and England starts at 9:30 am (IST). Enjoy !!!!

Bookmark this post: |

|

Unichem Labs

The stock jumped by 6.3% today to hit a CMP of 308.00 rupees. Consider exploring this stock for a buy.

Here's why -

a) The stock is available at a fwdPE of 12.36, which is one of the lowest amongst all pharma stocks

b) Although sales are growing slowly, the PAT is zooming at over 20% growth

c) The PAT per quarter has been in upwards of 18 crs over last 3 quarters

d) There is preferential allotment of shares to a private equity firm which has recently jacked up the prices. (the stock grew by 37% in two months)

e) The current dividend yield is 1.14% only. But given the increase in profits this year, I expect an increase in dividend to 5 rupees a share. It wont be more than this as the company is looking at expansion opportunities and acquisitions .. where internal accruals may be more handy than debt.

That apart, I found another swanky news item on Investsmartindia. Diabetes, Cardiology and Anti-infectives are growing areas in the healthcare segment. Buy in low numbers now and increase stake if it drops anywhere.

Bookmark this post: |

|

Saturday, April 1, 2006

It aint done till, it's done

The picture above is what provisionally sixth placed Giancarlo Fisichella saw, as P5 Jenson Button's engine blew at the penultimate turn of the Australian GP. Inspite of a blown engine, Button didn't remove the foot from the pedal in a serious bid to cross the line ... he finished a menacing 7 metres from the finish line. Ironically, Jenson Button started on pole position at the start of the race. News

Well (sob, sob ...) this is the second time, I've lost a bet because of engine blowups in the last lap of a race. The last occasion was when Mika Hakkinen's splendid drive around the 2001 Spanish circuit came to a close as his Mercedes engine gave way to a lucky Michael Schumacher.

Bookmark this post: |

|

Tuesday, March 28, 2006

Sandesh Limited

Sandesh Ltd. is available at 113.00 rupees (28-Mar).

Sandesh Ltd. has an NCAV of 111.45 rupees.

The scrip has cash per share of 26.60 rupees which is very good. It has a good market share in Gujarat where it is now the #3 newspaper (from #2, a year ago). At these numbers, prudence has it that the stock will go up however from an investing viewpt, the following needs a look into -

a) Sales have dropped; so have profits

b) Didn't declare any dividend last year

c) There was a sudden spurt in sales last yr (from nowhere we has a number of 635 crs in the financial statement)

d) Q3, 2005 was a negative profits quarter

e) Fwd PE comes to 17.20 (but very inconsistent profits)

So although this stock gives me fantastic margin-of-safety, it doesnt give me the comfort of a consistent and growing earnings growth. If anyone's been tracking this stock, then opinions are soughted.

Bookmark this post: |

|

Sunday, March 26, 2006

For just a penny more, or maybe a penny less

1. Abbott India is range bound. There is support for the scrip at 625 rupees and has a resistance at 700 rupees (level 1) and 725 rupees (level 2). The scrip is current available at 640 rupees. Advise punters to buy with a stop-loss at 620 rupees. The Q1 results of the company are due on 31st March 2006. There will be some traction in the stock then.

Fundamentally, profits have been lower than LY and at a CMP of 640, fwdPE comes at 16.12. The NCAV of the stock is 101.94 rupees. The company has declared a dividend of 17.5 rupees only (it was 35 rupees last year; the announcement came early this month .. and hence the rapid fall in value from 700 to 640. Yet the dividend yield stays at 2.76%). Sales are growing at 12% p.a., all quarters have been profitable (at over 10 crs a qtr) and management is good.

2. Helios & Matheson's stock value has been on a down trend due to a news item. Infact 13th Feb was a rather volatile day for the scrip. It opened at 220; reached a high of 254.90; fell to a low of 200 for the day and closed at 249.15. The news was w.r.t. to some arbitration proceedings over one of it's subsidaries vMoksha.

The company has a marginally negative NCAV. What's remarkable is the rising revenues and profits of the company which went up 90% and 140% respectively. My calculations of the fwdP/E come to about 10.58. Traders can look at an exposure in this scrip with a stop loss at 170 rupees.

There are a number of stocks which have seen a reduction in prices over the last one month or so, however you and I'll be comfortable with the one where fundamentally the stock is sound, while external events which can be controlled are responsible for the lowering in value.

Bookmark this post: |

|

Friday, March 24, 2006

The Framing of Decisions and the Psychology of Choice

The following text is an adaptation of a 1981 Science paper, “The Framing of Decisions and the Psychology of Choice” where Tversky and Kahneman presented a glorious example which delve in the psychology of making a rational decision among seemingly-diverse options.

Imagine the Avian flu disease has now been discovered in Sri Lanka and is expected to kill 600 people. Two alternative programs to combat the disease have been proposed.

1. Under Program A, a projected 200 people will be saved.

2. Under Program B, there is a one-third probability that 600 people will be saved, and a two-thirds probability that no one will be saved.

Which one will you go in for - Program A or B?

The researchers then restated the problem: this time, with -

1. Program C, “400 people will die”

2. Program D, “there is a one-third probability that no one will die, and a two-thirds probability that 600 people will die.”

Now, which one will you go in for - Program C or D?

PS: The authors observations are given in the comments. Please have your answer ready before peeking through the comments

Bookmark this post: |

|

Monday, March 20, 2006

It's getting better all the time

I'll be closing 2 years of investing on the equity markets this 31st March. Confession - I have made much less money than what an index fund would have given. But have learnt a lot in the process. How I missed many an opportunities? And again missed the same opportunities? When to sell and not to sell? Buy or not buy and buy how much? Im still ridden with a number of stocks which have dimished 40%+ in value.

OK, this may be amusing ... the first ever stock I bought on the equity market was Padmalaya Telefilms and this was also the very stock I sold off at a loss ... a loss of 63% from cost.

But the truth is: I am very much getting better at this. In evaluating companies, on the right time to buy, am seeing more in the B/S and P&L and the importance of news and volumes. My choices and recommendations in the last one month have been much better than ever before.

> Amtek India in 37 days, is up 18%

> Gujarat NRE Coke in 33 days, is up 10%

> Aftek Infosys in 3 days, is down by 1%

> Ind Swift Labs in 1 day, is up 16%

Bookmark this post: |

|

Saturday, March 18, 2006

News, prices and tale spin - Visualsoft Tech

Visualsoft Technologies Ltd. made a press release on the 17th of March, 2006 stating that - they are no longer going ahead with the amalgamation of the two other pvt companies with Visualsoft Technologies Ltd. Another relevant info in the same news item was - Mr. Sashi Reddy has resigned as the CEO of the company.

The charting below shows the performance of the stock.

The stock price has taken a serious dent from it's Jan4th levels of 260 rupees and is today almost 50% below that price. Notice the strong volume of 1.75 million on 17th March 2006 because of the news that the amalgamation has been aborted and the resignation of the CEO of the company. On that day, the stock fell from 162 rupees to 138 rupees.

Financially, the specs of the company are enclosed -

Share capital - 19.98 crs

Loans - 0.00 crs

Investments - 0.00 crs

Net current assets - 154.10 crs

FV - 10 rupees per share

Dividend - 2.50 rupees per share

CMP - 138.65 rupees per share (17-Mar)

LY profit - 28.34 crs

Lets make some inferences from this -

1. NCAV for Visualsoft Technologies is a fantastic 77.13 rupees/share (the CMP less than 2x of the NCAV)

2. Cash with the company is 54 crores i.e. 27.02 rupees of cash per share

3. Zero debt company (cash rich - zero debt is a lethal combination !!!)

4. Dividend yield would come to 1.79%.

Now the problem areas -

1. While sales in Q1 and Q2 increased by 14% and 15% respectively over last yr, the Q3 sales actually dropped by a huge 41% over last yr

2. Profits for Q1 fell by 24% over last yr, for Q2 fell by 6% over last yr and for Q3 fell by 41% over last yr

3. Estimated profit for the year is only 19 crores for the company which means a P/E of 14.72. (a P/E of 14 is available with other peers aswell who although donot have this fantastic NCAV that Visualsoft holds, but have more stable earnings)

4. The profits are well below my 10 crs per quarter rule.

5. and ... I have the slightest idea how the stock will behave over the next 3 days.

Mar-17 saw huge volumes on this counter and massive decline. March 20th can be a make or break. Amazingly, this is the same company which was listed in Forbes as one of the Top 200 Small Companies in the world.

Questions for you -

a) Is Visualsoft under / fairly / overpriced at rupees 138.65?

b) Will Visualsoft go further down in price over the next week or so? If yes, how much? If not, why not?

c) Is there some appreciation to be seen in the price of the stock over the next 3 months / 1 year from today?

An additional question - investing in which stock is preferable ... a Visualsoft which has a great NCAV but sparse earnings record or an NIIT Technologies which has no NCAV but a consistent and growing earnings record?

Bookmark this post: |

|

Friday, March 17, 2006

What a tip !!!

A friend called up this evening to discuss a tip he received from his broker - Buy Ramco Systems. The reason being - the stock is at it's 52-wk low of 193 rupees and it's 52-wk high was a huge 519 rupees. He said, the stock had mighty upside as buying levels will increase. I checked out the numbers and was absolutely taken aback with the financials. Enjoy this !!!

a) The company has been in the red for six out of the last eight quarters

b) The P&L account of the company shown a loss for the last 4 financial years

c) Personnel expenses account for 40% of the total sales of the company

d) No dividend for the last 5 financial years (obviously)

But that's not the shocking part ....

Check the prices over these last eight quarters. I have taken the highest price within one month of the close of quarter (these are the times when the financial statements come out)

Mar-04: Profit of 4.21 crs; Price was 265 rupees

Jun-04: Loss of 9.29 crs; Price was 250 rupees

Sep-04: Profit of 2.32 crs; Price was 290 rupees (the price increased while profits dipped)

Dec-04: Loss of 3.36 crs; Price was 440 rupees (the price increased while profits dipped)

Mar-05: Loss of 30.04 crs; Price was 425 rupees

Jun-05: Loss of 6.03 crs; Price was 405 rupees

Sep-05: Loss of 7.11 crs; Price was 450 rupees (the price increased while profits dipped)

Dec-05: Loss of 3.68 crs; Price was 330 rupees

From 13-Sep-2005, when the stock reached a high of 546.70 rupees ... it has been steadily declined and it today (22-Mar-2006) at 194.25 rupees. A decline in value of 64.46% in a little over 6 months. Amazing tip, aint it?

Bookmark this post: |

|

Ind Swift Lab

Ind Swift Labs moved UP by 15% today. I bought the stock yesterday.

It's not often that I write a statement like this. Fluke .... (no wait) ... big fluke !!!! ... not buying the stock, but the sudden jump

Share Capital - 20.90 crs

Loans - 145.35 crs

Investments - 3.14 crs

Net CA - 88.16 crs

FV - 10.00 rupees per share

Dividend - 1.50 rupees per share

CMP - 115.00 rupees (Mar-24)

LY Profit - 26.59 crs

Why I bought Ind Swift Labs?

1. I estimate a closing yr profit of 35 crs i.e. a P/E of 6.87.

2. Growing profits and sales for the last 5 years (YoY (04-05) growth in profits was 300% and sales was at 55%)

3. The sales growth numbers (qtr-on-qtr for 2004 and 2005) show a progressive story -

a) March - 45.22 crs v/s 83.22 crs (84% increase)

b) June - 44.00 crs v/s 79.97 crs (82% increase)

c) September - 45.48 crs v/s 80.28 crs (77% increase)

d) December - 66.75 crs v/s 82.36 crs (24% increase)

4. Profits have also moved in a positive direction, though not on similar constants - 251%, 18%, 21% and 418%.

5. Dividend yield is 1.30%. I expect a higher dividend payout of 2.5 rupees per share i.e. a dividend yield of 2.17%.

6. Excellent news value

7. The final blow was dealt by the charting of the scrip. Notice the fall in the share from 210 rupees, an year back to half that price today. The big avalanche started from Jan 18th (170 rupees) till it reached it's low of 97.60 on March-23rd (yesterday).

Please note that Grahamian numbers will not purport a buy for the stock because of the negative NCAV of 25.86 rupees, low cash in company and high debt. I find the management good, an enticing price even at 115 rupees (imagine, I bought it yesterday at 97 rupees) and excellent growth prospects.

Bookmark this post: |

|

Thursday, March 16, 2006

Savita Chemicals

Pl keep this scrip in your watchlist

I'll start with 'things-that-hurt' on this scrip. The stock -

a) Is rather close to it's 52-week high

b) Is below my 10 crs a quarter rule

c) Is fairly above it's NCAV (4x above)

d) No news value

Now, what I like about this stock.

a) Savita Chemicals has improved in sales and profits by 20% for the last three quarters

b) It's fwdP/E ratio is 11.08

c) The company hardly deploys debt in it's balance sheet .. just 20.24 crs

d) Cash in the company is 21.66 rupees per share. Not much, but good enough to convince me of another dividend ... of atleast 12 rupees.

e) Dividend yield would come to 2.33%

The charting of this scrip has me stumped. Savita Chemicals has virtually no volumes to speak off, however it has consistently grown in the stock market. Price on 16-March-2004: 100 rupees; Price on 16-March-2005: 235 rupees. Only one dip - in the month of Nov 2005 when it went down to 275 from 375. I feel the stock will fall down to 350 rupees and not more ... sooner or later. It might be a good idea to pick a small stake once the stock touches 375 rupees to a share.

Bookmark this post: |

|

When probability doesnt make sense

You enter your plush office this morning and are greeted with a phone call from your broker. He wants to play a game, and feels you are the right player for this little experiment. He explains the rules - you shall toss a coin and call for a heads or tail. If your call is correct, then i'll double the money in your wallet. However, if you call wrong then i'll halve the money. If you dont participate in this game, the eccentric broker would give you 100 rupees.

What he doesn't know is that he is dealing with a mathematics stud from your school days and such problems are small-fry for you. Being the champion of probability, you pick your pen and try to simulate the problem ...

a) You assume that you hold 1000 rupees in your wallet

b) If you call right, the 1000 rupees become 2000 rupees.

c) If you call wrong, the 1000 rupees is down to 500 rupees.

d) In both cases, the probability of the event happening is 0.5

Simple equation .... X = [probability of (1000)*two + probability of (1000)*half] - 1000

or, X = [(0.5)*2000 + (0.5)*500] - 1000

or, X = [1000+ 250] - 1000

or, X = 250

Brilliant, you say. X is 250 rupees which is greater than 100 rupees (for non-participation). So, I must participate. Its a clear arbitrage of 150 rupees.

Think a little further .... You've participate in the game based on this probability analysis. What next? .... The use of probability analysis to aid you in decision making of participation in the game is only secondary. What's more important is how probability helps you in arriving at the correct call so that you can double your money.

To illustrate, imagine you had called wrong. Your purse would have been lighter by 500 rupees, although your profound mathematical skills would beg to differ on your interpretations of loss.

OK, think still further ... the broker has tossed the coin which lands on his palm. He hasn't shown you the result. Remember, you have used your probability skills to arrive at the logic that you have 150 rupees of "free money" to be made by participating in the game. He now gives you a second chance ... he says "I give you an option for you to not take this fall of the coin. You can tell me to toss the coin again.". You do your round of mathematics again and arrive at the same 150 rupees advantage. This still holds true. But what is the use?

By now you would have realised that the deal was inconsequential when we used probability analysis to the problem. Perhaps, just taking the 100 rupees was a better deal.

Adapted from "The Two Envelopes Paradox" by Keith Devlin

Bookmark this post: |

|

There's something about Aftek

Aftek Infosys stats are enclosed -

Share Capital - 17.06 crs

Loans - 129.54 crs

Investments - 59.59 crs

Net CA - 374.40 crs

FV - 2.00 rupees per share

Dividend - 1.00 rupee per share

CMP (22-Mar; 10:05 am) - 78.45 rupees per share

LY Profit - 59.80 crs

Hence,

a) The NCAV (excl invt) comes to 28.71 rupees per share, which is quite excellent for an IT company (pl revert to the blog on Visualsoft Tech where Prasanth, Ravi, Rohit and me blew away the NCAV technique for evaluation of IT companies).

b) Sales and profits have been rising at 25-30% every year and this year is also no different.

c) Dividend yield comes to 1.30%

d) EPS comes to 7.01 rupees per share

Some other inferences ....

1. Loans are very interesting. Unbelievably, Aftek Infosys had been debt-free for the last 3-4 years. From nil debt last year to 129 crs this year would raise eyebrows. However, when I look at this number on the basis of capability to service debt ... the company is well on cue. At 129 crs, the interest cost would come close to 13 crs for the year (at 10%) and with the company earning 60 crs of profits per year, servicing this amount is not an issue (at an interest coverage of 4, the company would have a AAA rating with 150 crs of debt). The debt has been raised through the FCCB route.

2. I expect this NCAV to come down in the next annual report due to the major component of this NCAV is cash (328 crores or 38.45 rupees/share). Aftek would ideally be using this cash to acquire other businesses across the world. The fact that Aftek already has enough profits to take care of it's debt servicing, would mean it can deploy as high as 80% of this cash for acquisitions. If I assume 60% deployment, then the outflow of cash will be 196 crs or 23.07 rupees/share of cash. So the NCAV should come down to 14.86 rupees/share in the next annual report, ceteris paribus.

3. Consequently, investments would increase because of the increase in stake with Arexara Information Technologies Gmbh and V-Soft.

4. I expect a stronger dividend payout by the company inspite of the increase in share capital. The dividend payout may well be close to 75% for this financial yr which improves the dividend payout marginally.

5. The financial year has been changed, so it makes sense for us to see quarterly numbers. On this basis, I find that the fwdP/E of the company should come to 10.08 which is truly excellent.

Whats changed? ... see the charting below.

The stock seems excellently priced, a good management, concrete business plans ... all in the making of a good buy.

Bookmark this post: |

|

Wednesday, March 15, 2006

Pricol Limited

I examined the nine-month financial statement of Pricol Ltd.

In summary,

a) The sales have increased marginally (7.4%) over the nine-month period in the last FY (2004).

b) Correspondingly, the PBT have fallen significantly (from 43.9 crs to 28.6 crs; a drop of 34.8%)

c) Notice the rise in interest cost. The nine month interest cost is at 8.43 crs while the financing cost was 4.87 crs in the previous FY. (a 73% rise)

d) Net profit after tax, dep and interest (PAT) is at 22.9 crs while it was 28.09 crs for FY2004-05.

The balance sheet reads ...

Share Capital - 9.00 crs

Loans - 155.90 crs

Investments - 14.75 crs

Net CA - 86.13 crs

FV - 1.00 rupees per share

Dividend per share - 1.00 rupee

CMP - 39.75 rupees/share (15-Mar)

Thus, the NCAV (as per 2004-05 balance sheet would come to negative 7.75). Estimating trends in FY2005-06, I find ...

1. The profits for the year should be around 29 crs. This would mean a P/E of 12.08 on todays CMP.

2. There is no margin of safety here. The NCAV is infact, negative.

3. The company would be in a position to give a dividend of 75 paise only this yr due to the lower earnings. This comes to a 1.89% dividend yield.

4. There is no news of value on the stock too - although it has decent volumes on the bourses.

My take - this stock will not move much from this level for the next few weeks. Further improvements in the stock price will be a function of news or increase profitability. There is no hidden value in the stock that is visible.

PS: I think the company is resorting to some creative accounting practices here. Picture this (look at the annual report) -

> In 2003-04, the company had borrowings of 115.23 crs on 31-Mar-2004 and had accounted for an interest cost of 8.02 crs. Which means we are looking at a financing cost of 7.5%. Fair.

> In 2004-05, the company had borrowings of 155.90 crs on 31-Mar-2005 and had accounted for only 6.83 crs .. a financing cost of only 4.4%. At 7.5%, this should have been around 11.69 crs.

> For 2005-06, the interest cost would close at close to 13 crs. I would like to assume that the increased financing cost is making up for the lower accounting of interest cost in the previous financial year. So, loans would not have increase too much this year. Lets estimate it at around 160 crs.

Bookmark this post: |

|

Tuesday, March 14, 2006

Fantastic P/E ratios ( .... low, figuratively !!! )

You might want to research some of these stocks. They have a fairly good market capitalisation and a rather strong P/E ratio amongst their industry peers. I found these in some old files .. seems to be January 2006 data.

I have marked the ones which have shown increasing Q-on-Q profits over the last three quarters in green for your reference. We'll evaluate these over the next two weeks.

Madras Aluminium [12.58]

Pheonix Lamps [10.78]

Pricol [10.58]

Eicher Motors [2.78]

Ashok Leyland [13.48]

Punjab Tractors [10.86]

Bank of Baroda [12.17]

Federal Bank [5.65]

SBI [10.02]

Jupiter Biosciences [6.65]

JK Lakshmi Cement [10.11]

Everest Industries [9.33]

Gujarat NRE Coke [7.42]

India Glycols [6.17]

Savita Chemicals [9.35]

Jaiprakash Associates [13.02]

Nava Bharat Ferro [6.45]

Havell's India [17.09]

LG Balakrishnan [16.09]

Kirloskar Oil Engines [6.50]

GNFC [6.59]

GSFC [6.25]

Mangalore Chemicals [5.85]

GAIL [9.86]

Mascon Global [11.79]

Tata Elxsi [19.22]

Tinplate [5.30]

Adani Export [12.46]

Atul [12.35]

Dredging Corporation [11.79]

Gujarat Alkalies [4.84]

MIRC Electronics [7.23]

Su-Raj Diamonds [7.95]

LIC Housing Finance [9.34]

Shriram Transport [8.42]

Tata Investment Corp [8.90]

ONGC [11.07]

JK Paper [7.97]

West Coast Paper [7.11]

Rallis [9.38]

IPCL [5.30]

Ind Swift Lab [8.18]

Aarti Drugs [9.06]

Merck [11.99]

Shasun Chemicals [13.71]

Torrent Power SEC [8.73]

Infomedia [8.14]

Bongaigoan Refineries [7.00]

Chennai Petro [5.14]

Mercator Lines [4.82]

Varun Shipping [5.77]

Bhushan Steel [4.30]

Monnet Ispat [6.40]

Essar Steel [1.58]

Lloyds Steel [1.78]

Mukand [2.61]

SAIL [4.15]

Mawana Sugar [12.51]

Avaya Global Connect [13.94]

MTNL [10.96]

Alok Industries [10.74]

Nahar Export [6.56]

KEC International [4.58]

Apollo Tyres [14.96]

Bookmark this post: |

|

Monday, March 13, 2006

What are the odds? (South Africa - Australia)

.... and still have to bite the dust

Bookmark this post: |

|

The greatest cricket ODI ever played

Bookmark this post: |

|

Sunday, March 12, 2006

Venus Remedies

2. GM Breweries

Venus Remedies was a turnaround story (sort of) and hence commanded Stockpaisa.com's patronage as the stock-pick. A quick-peek of GM Breweries reads a similar story.

a) LY sales were 104.33 crs; this year the company may close with 155 crs

b) LY profits were at 0.75 crs; this year the company should close at 9 crs

c) Again, an NCAV one would have zero comforts on (negative 22.84)

d) Surprisingly, this company doesn't subscribe to making many an announcements as in the case of VR.

I would again quantify this stock as a may-be-superhero stock and is more for aggressive investors and not conservative ones like myself. The price target given by stockpaisa.com for this stock is 120 rupees in the 3-5 month horizon.

The stock did reach a high of 89.35 rupees to a share and is currently at 71.2 rupees. The 52-wk low is 16.60 rupees/share. The charting of the scrip shows some inconsistent volume movement. The current trend shows that volumes are a bit on the decline .. but this can abviously change anytime.

3. Areva T&D India Ltd.

When I last researched this stock (Feb 25), the stock price was 468.00 rupees. I found it a bit expensive then. Today it is at 746.40 (Mar 10). The stock jumped 59.6% in 15 days.

Lets examine the stock stats -

Share capital - 39.89 crs

Loans - 1.58 crs

Investments - 9.65 crs

Net CA - 128.38 crs

FV - 10.00 rupees per share

Dividend - 1.75 rupees per share

LY Profit - 21.20 crs

Est profit for this FY - 50.00 crs

CMP - 743.00 rupees per share

On the basis of the above -

a) NCAV of 34.21 rupees / share

b) Dividend yeild of 0.24%

c) fwdP/E of 59.28

Any news value? Heavy ... the group is hiving off it's motor business, amalgamation etc. The company has some very good sales and profits to show for the last 3 quarters. The current volume trend suggests a little further movement up in the stock before a possible correction (afterall a P/E of 60 might be a bit difficult to sustain esp. when the industry is at around 34 levels)

Bookmark this post: |

|

Saturday, March 11, 2006

Property wisdom

"The whole of Delhi is into properties", said the property broker, who took me for a spin this Saturday. Clever buggers these guys ... they'll do their best to ensure that he thinks my money as his onw, he would say that he'd sell our flat to another buyer at a little higher rate (it's another story that he might do the same thing to me aswell) .... that's their way to gaining confidence. Traits of a professional salesman.

Some tips I could remember -

a) Always go in for smaller property sizes as compared to bigger property sizes. It's easier to sell and often has the best appreciation in value

b) Plots are preferable over flats if quick returns are your goal. Plots are easier to sell as compared to flats.

c) In flats, the variation in prices is not as much as compared to plots, where location and frontage is of primary significance

d) If you are searching for one (plot/flat/house), there will always a second broker who would give you a better deal. So search more, and seek more.

Bookmark this post: |

|

Friday, March 10, 2006

Stock picks by Stockpaisa.com

Stockpaisa.com has given it's list on price targets in it's website. The list has been worked keeping positive ripples from the budget into perspective and the technicals / fundamentals of the company.

The top five in the list with expected returns over the next 3-5 months are -

1. Venus Remedies - 61%

2. GM Breweries - 58%

3. Areva T&D India Ltd. - 54%

4. Astra Microwave Products Ltd. - 49%

5. Flex Industries Ltd. - 49%

Let's examine a few of them in this post -

1. Venus Remedies

VR is not a Grahamian stock, by a long shot. It's NCAV is at 5.76 while it's CMP is at a fairly high 363.00 rupees per share. With a dividend yeild of 0.28%, I was kinda wondering what makes this stock command such a high valuation. That was when the news element of the stock bundled me ....

a) 12-Dec: VR in talks with MNCs over drug licensing (Cephalosporins combination)

b) 15-Dec: VR has appointed a senior scientist

c) 16-Dec: VR sets up wholly owned subsidary in Germany

d) 27-Dec: VR broad bases Board

e) 3-Jan: VR filed third PCT International Application

f) 17-Jan: Venus Remedies up on Q3 (we'll examine this aswell)

g) 31-Jan: VR acquires pharma unit in Germany

h) 20-Feb: VR filed fourth PCT International Application

i) 8-Mar: VR to consider issue of FCCB

Financially, here's where the company stands -

a) On profits - LY profits were a miniscule 4.1 crs. However this year has been a different story. Q1+Q2+Q3 profits currently stand at 10.81 crs. Extrapolating the numbers, the profit for the year should be on around 16 crs. Which means an EPS of 24.96 rupees/share.

b) The fwdP/E of the stock is at 14.54 which is fairly lower than other emerging pharma companies

c) Sales are going at a doubly pace (a bit more than that) ... LY sales were at 30.83 crs while this year (in 3 qtrs), the company has reached 62.06 crs. At this scoring rate, the company should close at around 90 crs of sales for this FY.

Now, what makes me think again ....

a) All this news ... where did this come from? You might want to read the announcements in BSE. Venus Remedies has close to 50 announcements at the BSE in the last 365 days. (Dr. Reddy's had around 60 announcements in the same period)

b) There is no margin of safety in the stock for comfort. At an NCAV of 5 and a book value (LY) of 23.55 rupees per share ... a CMP of 363 would mean .... (both LY numbers)

1. P/BV ratio of 15.41 and,

2. P/Sales ratio of 7.5

c) And ofcourse, you know my disapproval to any stock who would not give me 10 crs of profit to the quarter. VR is well below that mark.

However, this is not to dissuade you from purchasing the stock as a not-that-far-feteched-bet. The big question is ... when to buy and how does this stock move. Answers to this can be obtained from the charting given below. Interesting trends, these ...

The stock first started moving in the September of 2004. It moved for 4 months (till Dec 2004), post which the stock was silent for 5 months. Again in May-2005, huge volumes moved up the stock to touch 300 rupees per share. This continued for 4 months (till July 2005), post which a lull set in for another 5 months. Another spurt has been seen this Dec onwards. It's been on for Jan, Feb and Mar ... 4 months again. What's your take for the next 5 months?

Bookmark this post: |

|

Meaningful answers

Which drink tastes better - Coca-Cola or Pepsi? In a recent focus-group discussion, a market research company asked this question to a 100 people and of them, 90 said Coca-Cola while 10 said Pepsi. To further understand if people are able to distinguish between the two drinks on the basis of it's taste, the agency asked 5 volunteers from the "i-love-pepsi" group to sip 5 bottles of the blank-labeled cold drinks presented to them, and tell us the right drink. Amazingly in 4 out of five occasions they got it right.

Conclusion : 80% of all people are able to identify the taste of the drink they are having and 90% say Coca-Cola is better.

Let's revisit this - 0.8 is the probability of a person identifying the right drink which means he/she has a 0.2 probability of doing the opposite (reading the wrong drink). Which means, of the 90 Coca-Cola afficionades, it's possible that 20% of them would have got their taste wrong i.e. although they say "I-love-Coke", they would have selected Pepsi from the draw. Simialrly, the Pepsi group of 10 would have 2 people who would have tasted a Coca-Cola as the superior taste. So we have 16 "CC to P" people and 8 "P to P" people = 24 "I-love-Pepsi" people

Or, not 90% of the people love Coca-Cola but only 76%. And Pepsi goes up from 10% to 24%. Consequently, the probability of a Pepsi lover choosing a Pepsi from two drinks after sipping it, is only 8/24 = 0.33

Bookmark this post: |

|

Thursday, March 9, 2006

Player 1 v/s Computer

This isnt a Playstation game or the latest version of International Cricket Captains (ever tried this computer game .. it's amazing !!!). Just an extension of Devlin's piece on "A Game of Numbers". Devlin in this treatise has described how Oakland Athletics won the Western division of baseball in 2000, 2002 and 2003 with a team which had no 'A' cat super-stars ... a team which was just a summation of individuals with specialised skills.

Here's how they did it -

a) The initial premise was that unlike football (american style), baseball didn't require excessive teamwork. The pitcher pitches depending on his individual skills, the batter plays using his own skills and the out-fielder fields the ball unguided by other individuals. This is somewhat similar to what happens in a game of cricket.

b) Over time some 11 million batter-pitcher confrontations have occurred in 150,000 games. Thats a world of data to analyse. Coupling this data with random elements of pitches, weather, toss etc. you can create patterns w.r.t. which position to send each batsman, batsman can play a spinner or a faster bowler better, condition training schedules accordingly, individual tactics, patterns on how a bowler balls his first two balls and the last two balls (i've always noticed that the first two balls of any pace bowler are never the slower ball) etc.

Reading the article I came across some really wonderful notes, worth putting down here -

1. Batting averages are now generally regarded as a poor guide to performance - not least because they do not distinguish between a single, double, triple, or boundary; or how many players scored runs on a mis-hit or after being dropped or narrowly escaped being out.

Also, averages are rather misleading. Analyse this -

In the 1997 season, Jacques Kallis played 14 matches and scored 560 runs while Rahul Dravid played 35 matches to score 1350 runs. Assuming both got out on all occassions, the averages for the two batsmen are - Kallis - 40.00; Dravid - 38.57 ... So Kallis was better than Dravid for the 1997 season.

In 1998, Kallis played in 30 matches to score 1000 runs (at an avg of 33.33) while Dravid featured in 16 matches to score 500 runs (at an avg of 31.25). For the second time, Kallis beats Dravid with a better average.

Now, just combine the numbers. So,

Kallis ........ Matches = 44 (14+ 30); Runs = 1560 (560+1000)

Dravid ..... Matches = 51 (35+16); Runs = 1850 (1350+500)

Relook the averages .... Jacques Kallis is now at 35.45 runs/match while Rahul Dravid has an average of 36.27 runs/match. Hence Dravid is a better pick (and averages is not as powerful a statistic as is expected to be)