Its often a good idea to see what mutual funds are buying or selling these days. This helps you predict stocks which have a higher propensity of taking the dive or perhaps, soar the skies. I used MutualFundsIndia to list the top 4 performing funds over the last 3 months .. here's their list -

1. Deutsche Alpha Equity Fund - 37.35% in last 3 months

2. Sundaram Select Mid-cap Fund - 33.10% in last 3 months

3. SBI Magnum Comma Fund - 32.90% in last 3 months

4. Franklin India Opportunity Fund - 32.10% in last 3 months

Now, I guessed that the portfolio composition of all these 4 funds would tend towards parity or perhaps, a high correlation. If not companies, atleast the sectors. Here news -

1. Deutsche Alpha - Diversified (29%); Computers (9%); Metals (8%) ... top 3 cos: Sterlite (8%); Tata Steel (8%); Tata Chemicals (7%)

2. Sundaram Midcap - Engineering goods (17%); Housing (11%); Auto & ancillaries (11%) ... top 3 cos.: Kalpataru (4%); Balrampur Chini (4%); Ansal (3%)

3. SBI Magnum - Cement (14%); Diversified (13%); Metals (12%) ... top 3 cos: Hindustan Zinc (8%); Shree Cement (7%); United Phos (5%)

4. Franklin - Entertainment (22%); Auto & ancillaries (14%); Diversified (11%) ... top 3 cos: TVS Motors (9%); Jaiprakash (7%); Calcutta Electric Supply Co. (7%)

Amazingly ...

i) The top three sectors among the four top performing funds is strewn over 8 different industries (from a max:12)

ii) The top 3 holdings of each of the 4 funds is different i.e. we have 12 different companies that form the top 3 holdings of these 4 funds.

iii) The average holding in equities from the total corpus is a healthy 94%. (so you might want to rethink your idea of staying 60% in cash and rest in equity)

Mutual funds donot think alike and have different priorities and basis of evaluating stocks. For us the advantage is in identifying changes in portfolio in mutual funds to understand what they are buying or selling, researching the same and arriving at a decision.

PS: Has anyone checked the Calcutta Electric ... ???

Sunday, April 30, 2006

Mutual funds and stock valuation

Bookmark this post: |

|

Nahar Industrial Enterprises Limited

Nahar Industrial Enterprises Ltd. The company results have been very impressive over the last 3 quarters -

Jun-05: Sales increased to 176 crs from 90 crs LY; profits up from 3 crs to 14 crs

Sep-05: Sales up from 82 crs to 172 crs; profits rose from 7.12 to 15.07 crs

Dec-05: Sales upto 169 crs (from 156 crs); profits up from -0.72 to 18.26 crs.

Extrapolating these numbers over the next 3 quarters puts the fwdPE of the company at a powerful 8.56. I also find that -

1. The organisation's interest cost has been decreasing over the last few quarters, which is brillant. (there is one news item however, which indicates that the company is in discussion for issue of FCCBs)

2. The NCAV of the scrip is 13.92 with a sizable investment head of 66 crs in the balance sheet (mostly owing to shares in sister concerns - NSML and NEL)

3. A visible increase in net margin from -1.5% in FY2004, 3.3% in FY2005 and 9.2% till Dec-05

4. Surprisingly, no dividend has yet been issued although the company has enough cash reserves and cash profits.

5. The 31-Mar-05 book value is a comfortable 175 rupees/share

I would love to buy this stock. The only hitch on the charting is : the scrip had just created a valley a few days back when it dipped from 170 rupees to 130 rupees. It's now back to 170 rupees. Dont risk market timing ... buy a small number of shares, buy more on declines.

Bookmark this post: |

|

Saturday, April 29, 2006

Alembic Pharma

Watch out for this stock. I advice BUY on declines in the price of the stock. Reasons -

1. Alembic has come out with a good Q4 result, displaying a strong increase in PAT (from 6.36 crs to 17.10). This is in line with earnings over the last few quarters.

2. The yr has closed at an EPS of 28.36. With the CMP at 401 (29-Apr), the PE comes to 14.13.

3. Sales have risen by 20% plus on every Q-on-Q results and so have profits. A lil' extrapolation would put Alembic's next 2 Qs results at a strong footing equaling around 16 rupees in EPS. I would picture Alembic at a fwdPE of 12.9 which is one of the lowest in the Indian pharma space.

4. The heavier part of the sales growth has come from domestic sales (around 77%) however interestingly, Q4 has contributed one-third of the entire export pie. This marginally indicates a move towards ramping export operations by the company.

A 99 yr old company, stable sales and profits, growing, a relative inexpensive valuation to peers ... worth a buy.

Bookmark this post: |

|

Wednesday, April 26, 2006

National Organic Chemical Industries Limited

or NOCIL for short. NOCIL is a turnaround story ... refered to BIFR in Jan-2004, it came out of bankruptcy with a positive net worth on 31st March 2005. The company had a fantastic 3rd quarter with an impressive 23 crs of profits on a capital base of 160.79 crs. Over the last 9 months, the company has notched up 59.50 crs of profits and should close at around 80 crs for the yr. The fwdPE of the stock would be a comfortable 5.63 - an alice in wonderland situation !!!

And although the company doesn't provide for any dividend, I take comfort over the fact that NOCIL has an NCAV of 4.07 and a book value of 10.90 (as compared to a CMP of 28.25). The high court has approved of a demerger of the company in two divisions to which the shareholders will benefit as the rubber division will take advantage of an independent management.

Peers of NOCIL would be other petrochemical companies like Castrol, Manali Petro, Narama Chematur, Hind Flourocarbons, Sah Petroleum, SA Petrochem, Lanxess ABS, Chemplast Sanma, Jubilant Org, DCW, IPCL and Finolex ... (barring Sah whose profits are almost non-consequential, NOCIL and Narmada Chematur exhibit the best improvements in qtrly earnings ... Narmada Chematur has also been recommended for a buy in a previous blog).

I would place a BUY on NOCIL with a stop loss on 24 rupees.

Bookmark this post: |

|

Nahar Export revisited

Nahar Exports Ltd has informed BSE that ....

Thus upon sanction of the scheme shareholders of the Company holding 100 Fully paid up equity shares of Rs 10/- each on the record to be fixed for the purpose, shall receive 55 Fully paid up equity shares of Rs 5/- each in NSML (post demerger of investment business) and 70 Fully paid equity shares of Rs 5/- each in the Company.

Questions -

1. Any arbitrage?

2. short/mid/long term prospects?

There was one report by EmKay which talks of latent (and now exposed) shareholder value in this deal. Here's how ...

1. The invt business in NSML (Nahar Spinning Mills Ltd.) is worth 346 crs which'll be merged with NCFSL (Nahar Capital and Finance Services Ltd.). Allotment ratio: 1 equity share of NSML = 1 equity share of NCFSL (FV Rs 5) + 1 equity share of NSML (FV Rs 5)

2. Textile business of NEL (Nahar Export Ltd) to be hived off and merged with NSML. Allotment ratio: 100 shares of NEL (FV Rs 10) = 55 shares in NSML (FV Rs 5) + 70 shares NEL (FV Rs 5)

The investment summary presented : a sum-of-its-part valuation of NEL gives Rs. 112 as the fair value of the stock. Hence the potential upside of NEL is 38%. (for a copy of the report, kindly email me)

Bookmark this post: |

|

Sunday, April 23, 2006

Paper

Surprisingly, the paper industry has been an underperformer. It's PE ratio has often been between 5 and 10, which is mighty lower than most other core industries. .. but things are looking better for this industry (story). An 8% growth in GDP means an 8% plausible increase in demand for paper, while the production is expected to grow at only 4%. This would lead to a rise in prices and hence profitability. Also, there will be consolidation in the industry with the smaller players merging with bigger ones (primarily due to the introduction of environmental norms). Players are also getting ready to explore the export market with 10-12% of the produce leaving Indian shores. (This would fuel prices even further)

Lets examine the prospects of a few players -

[1] West Coast Paper Mills Ltd. - The lastest quarterly data pegs the company at 537 crs of sales and 42 crs of profits. At a CMP of 393 (21-Apr), the PE is at 8.37. The company has also indicated an improvement in the net margin owing to cost control measures (and inspite the increase in fuel costs). It's a BUY candidate.

[2] Andhra Pradesh Paper Mills - I bought this a week back at 120 rupees. It's at 140 rupees today (21-Apr). The scrip has a fwdPE of 10.11. A recent report by EmKay Research gives the following cues -

a) Margin will double from 13.5% to 26.2% in the next two years

b) A 125% improvement in PAT over the next two years. In fact at today's price, the research agency estimates the stock to reach a PE of 4.4 by FY2008

c) Sales growth at a CAGR of 15.20%

d) The price target for Andhra Paper Mills is INR 224.00 (an increase of 76% from current levels)

[3] JK Paper - Here's another research report by Religare Securities Ltd. The CMP of JK Paper is 60 and it has a price target of 96 rupees. I'd however, prefer Andhra Paper Mills and West Coast over JK Paper as the company has shown a lack of consistency in profitability (profits went down by 8% last yr and sales were stagnant)

[4] Star Paper - Here's a pick of the week by icicidirect.com. Star Paper Mills has perhaps the lowest PE valuation in the paper industry ... a fwd PE of just 6.20. The company has shown brillaint improvement in sales with one glitch in the quarter ending Dec-05, where PAT was only 2.40 crs ... a huge reduction over last yr. So any investment in the scrip can be recommended only after checking the Mar-06 results of the company.

So here it is ... divide you paper industry booty equally between West Coast Paper and Andhra Paper Mills. They are a t good valuations, have grwoing sales+profits and good management structures.

Bookmark this post: |

|

Saturday, April 22, 2006

God knows why but my broker friend is extremely bullish on ...

In a recent post, Amit had penned the following comment :

Hello shankar,

My broker is extremely bullish on jHUNJHUNWALA VANASPATI.This stock has been hitting circuits for the past some time,the current market price(at todays circuit) is 58.He expects it to reach a three figure mark in a months time(atmost).

One other stock is UB enginerring trading at 63(todays circuit) which has also hit circuits almost daily in the past few days....

Will look forward for your advice on UB Engineering and JHUNJHUNWALA VANASPATI.

God knows what but my broker friend is extremly extremly bullish on JHUNJHUNWALA VANASPATI.

Best regards,

Amit.

Jhunjhunwala Vanaspati has risen from 40 rupees (Mar-28) to 65 rupees (Apr-21) - a return of 62.5% in 3 weeks [Charting]

On a more sanely and boring front, lets examine the financials of this scrip -

1. The stock is at a fwdPE of 6.12

2. Has been profitable over the last 5 yrs and all quarters are in the black (this isn't some small company .. it has sales of almost 500 crs)

3. Although quarterly profits are not high .. the company should close the yr with 10 crs of PAT

I would advice a small sum of money (not to be entirely taken as a gamble) ... towards this company. Keep a stop loss of 50 rupees however.

UB Engineering was at 32.95 (Mar-28) and has risen to 66.00 rupees (Apr-21) without a single day of negative returns .. one reason why Amit has not been able to lay his money on this stock [Charting]

UB Engineering has been posting losses for the last 4 yrs. One reason for recommending this stock can be the expectation that UB Engineering will be in the black this quarter like the previous one and perhaps actually, have had made some money. I would advice a "no buy" on this scrip.

Bookmark this post: |

|

Abhishek Industries

The Trident Group came as a shocker for the PGPM 2000-2002 batch of MDI, Gurgaon. The year was perhaps the worst, in salaries given to B-school students. Companies, on the other hand, were having a wonderful time picking students at dirt cheap packages. (I started at a take home of 19k p.m. which incidently, was higher than batch median ... whatever the tabloid might have said). Trident entered the campus as a Day 3 company and offered a package of 38,000 rupees p.m. .... a package that even batch toppers were deprived of.

The financials of Abhishek Industries :

1. The sales and profits have grown at 25% over LY and the Q-on-Q numbers have been impressive

2. I expect a closing of 51 crs for this yr ... an EPS of 2.62 rupees/share and a P/E of 11.35 which is much lower than competitors like Welspun India whose PE is at around 22.

3. A little high on debt, but has a good BV/share of 14.6 rupees

4. Two small hiccups .. Abhishek has not given a single dividend in the last five years and, has a negative NCAV (am not giving too high a priority to this however)

Abhishek Industries is a fantastic candidate for "buy and hold". The downside in the stock is minimal and has an excellent management team. The annual report (pdf, 6.20 MB) of the organisation calls for an excellent reading (dont miss the managements' discussions and analysis part .. pgs 46-57).

I would throw a buy on Abhishek Industries .. to be held for long.

Bookmark this post: |

|

Scrips I don't like

4 codes ... Buy / Wait / Pricey / Penny ... is what I use in my stock tracker.

Buy means an under-valued stock

Wait means a stock, fairly valued .. yet in contention if the price reduces

Pricey is a stock, over-valued and hence, not in contention yet

Penny is the scum-stock ... ones I'll stay away from for a long time

Here's a list of some I've classified as "Penny" (some changes may be done from this list on account of fundamental changes to the scrip) ... the primary reason for not investing in these stocks is the low profit levels exhibited by the below stocks

Silverline Technologies Ltd.

Tele Data Informatics Ltd.

Jindal Worldwide Ltd.

Shyam Telecom Ltd.

Vardhman Spinning and General Mills Ltd.

Saurashtra Cements Ltd.

Rain Commodities Ltd.

Morarjee Realties Ltd.

Selan Exploration Technology Ltd.

Prakash Industries Ltd.

Birla VXL Ltd.Mysore Cements Ltd.

Andhra Cements Ltd.

LML Ltd.

Moschip Semiconductor Technology Ltd.

Andrew Yule & Company Ltd.

IFCI Ltd.

Consolidated Finvest & Holdings Ltd.

FCGL Industries Ltd.

Sterling Holiday Resorts (I) Ltd.

Sharyans Resources Ltd.

Gujarat Sidhee Cement Ltd.

Swan Mills Ltd.

Premier Explosives Ltd.

Jay Shree Tea & Industries Ltd.

Ruby Mills Ltd.

Bhansali Engineering Polymers Ltd.

Mahindra Gesco Developers Ltd.

AVT Natural Products Ltd.

Suprajit Engineering Ltd.

J K Industries Ltd.

Agro Tech Foods Ltd.

Liberty Shoes Ltd.

Polyplex Corporation Ltd.

Sirpur Paper Mills Ltd.

Shriram Overseas Finance Ltd.

Gujarat Apollo Equipments Ltd.

Forbes Gokak Ltd.

Samkrg Pistons & Rings Ltd.

Himachal Futuristic Communications Ltd.

Empee Sugars and Chemicals Ltd.

Energy Development Company Ltd.

Aksh Optifibre Ltd.

ABG Heavy Industries Ltd.

UTV Software Communications Ltd.

Yokogawa India Ltd.Prime Securities Ltd.

Cyber Media (India) Ltd

Eimco Elecon (India) Ltd.

Harrisons Malayalam Ltd.

Kalyani Forge Ltd.

Venky''s (India) Ltd.

Revathi Equipment Ltd.

Standard Industries Ltd.

Sarla Polyester Ltd.

Themis Medicare Ltd.

Goodricke Group Ltd.

Ramco Systems Ltd.

Nesco Ltd.

Om Metals Ltd.

Z F Steering Gear (India) Ltd.

Texmaco Ltd.

Star Paper Mills Ltd.

Madhucon Projects Ltd.

Transgene Biotek Ltd.

Indian Hume Pipe Company Ltd.

Central India Polyesters Ltd.

Swaraj Mazda Ltd.

Anant Raj Industries Ltd.

Ondeo Nalco India Ltd.

Scooters India Ltd.

International Travel House Ltd.

State Trading Corporation Of India Ltd.

Megasoft Ltd.

Spel Semiconductor Ltd.

Saregama India Ltd.

Faze Three Ltd.

Eskay Kn''''''''IT (India) Ltd.

Kale Consultants Ltd.

Force Motors Ltd.

S B & T International Ltd.

Deepak Nitrate

Mather and Platt (India)

Excel Industries

Bharat Gears

Triton Valves

Liberty Phosphate

Advanced Micronics

Bookmark this post: |

|

Monday, April 17, 2006

Torrent Power SEC Limited

After living in Delhi - Ahmedabad and Surat came a great respite .. from power cuts. The AEC (Ahmedabad Electricity Company) and SEC (Surat Electricity Company) are governed by Torrent Power and both stocks have good valuations .... SEC being the better half.

1. SEC gives upwards of 10 crs every quarter and would close the year at 60 crs.

2. The stock is available at a fwdPE of 9.15 which is pretty good.

3. The energy sector is on an upscale and Surat's energy consumption is surely on the rise ... aren't you hearing news on textile and diamonds more often ... ?

One pt. - the growth of the company will be dependent on the geographical spread. So although I see an upside to the stock ... maybe hitting 720 rupees in the next 3-4 months ... further holding will need to be checked with every quarter.

Bookmark this post: |

|

Sunday, April 16, 2006

Hexaware Technologies

Hexaware is a global provider of IT and Process outsourcing services with presence in the Americas, Europe and the Asia Pacific region. The company has an active base of over 100 clients and has companies like Peoplesoft and SAP as partners. It operates in the HR outsourcing space. Net net, Hexaware is a new-age technology company ... and ... the valuation is very interesting. Measure this :

1. Revenues have grown by 24.3% over LY and is now at INR 678.6 crs (press release)

2. PAT grew at 43.6%; now at INR 91.4 crs

3. 39 new clients added; 129 active clients

4. At a CMP of 150 (Apr-15) and a share capital of 23.48 crs (FV per share is 2.00 rupees) ... the P/E comes to 19.13.

The company has given a guidance for Q1 FY2006: 167 crs in revenue and 23 crores in profits ... which spells the growth objective of the organisation. Extrapolating the expected growth in business (as a function of manpower recruited, clients added, previous trends), I find the company well on course to reach a 1000 crs of revenue by 2008. Thus, profits will also rise at a CAGR of 27%. I estimate the 1-yr fwdPE at 16.6 which is much lower than peers such at 3i and Matrix.

Hexaware Technologies is a long-term buy.

Bookmark this post: |

|

Saturday, April 15, 2006

AVP

Alien v/s Predator is a Hollywood flick where a team of archeologist discover an Aztec temple under the Antarctic circle, housing a host of alien creatures .. none better than the Alien family and that of the Predator lineage. Only one will win.

A similar comparison can be made in IT stocks .. the biggies .. esp. after the wonderful guidance given by Infosys Technologies Ltd. a couple of days back. I put four IT companies to the test - Infosys Technologies, Satyam Computers, TCS and Wipro. All the above companies have a m-cap of over INR 25,000 crores and have over INR 750 crores of LY profits. All carry virtually zero debt in their balance sheets, are cash-rich businesses and have strong management. And yet there are a number of differences which can be analysed and exploited -

1. Growth in profits has been rather different for all 4 companies. I find that TCS has shown the fastest growth in profits over LY at 42%, while Infosys has been the slowest with only 16% growth. (Satyam - 20%; Wipro - 31%)

2. CMP/NCAV would mean the "margin of safety" that Graham has so often cited in his many illustrations. The ideal number is 0.66. However this number is more true for old economy businesses and not for new sector business like IT services. For the record, Satyam is the best here with 8.66, while TCS has 37.79. (Wipro - 19.73; Infosys - 21.95; NCAV includes investments too)

3. At current prices, I estimate the fwdPE of all four companies at - Satyam - 27.91; Infosys - 37.38; Wipro - 37.81; TCS - 33.31

4. Cash per share - Satyam is at #1 with 75 rupees/share while Infosys is #2 with 54 rupees/share

5. While the dividend yeild of all 4 players is below 1%, Wipro is the best of the lot with a 0.96% dividend. Infosys however just pips Wipro with the special dividend of 30 rupees/share declared recently.

Examining these numbers, I feel Satyam is a good buy at the current price. There is an expectation of a bonus issue from Satyam aswell or a big dividend (it has crazy amounts of cash and is not eyeing any acquisitions).

PS: The movie was pathetic !!!!

Bookmark this post: |

|

Wednesday, April 12, 2006

Why panic?

The sensex fell 300 points on 12th April and another 100 points on 13th April ... and people are saying all kinds of things. Some important facts -

> the market has gone down by just 3.44% over the last two days. This is much better than those days when some of our stocks have gone down by 10% or more.

> a 400 pt drop reduces the current sensex P/E by almost hundred bps. So this should be at 19, right?

> corporate profits have improved over time ... nothing drastic has happened in terms of reduced exports, still higher fuel prices (it's remained the same over the last three quarters), global downturn. Infact exports have jumped, global economy is also on a high, real estate, gold prices and commodities are increasing .. things are getting better. Now an improvement in corporate earnings by 10%, would result in a reduction of PE by 180 bps. So your PE will go down to 17.20. If corp earnings is up 15%, then PE is 16.35.

It's my opinion, that the market will be upto 12000 by the end of May. Watch !!!!

Bookmark this post: |

|

Tuesday, April 11, 2006

Bloddy coincidence

I maintain a fairly extensive stock tracker which gives me a decent idea of NCAV, P/E ratio, fwd PE, debt recap numbers etc. Two stocks - Aarvee Denim and Exports Ltd. and Nahar Exports - are listed sequentially there. Surprisingly ...

1. Both stocks have an m-cap of 290 crs

2. Both stocks give a dividend of 1.50 on a 10 rupee share

3. Both stocks have similar debt recap value of 105 crs and consequently, the same ratio of debtrecap/m-cap

4. Both stocks have the same fwdP/E ratio of 7.90

I had put Nahar Exports on the BUY list a month back when it was at 70.00 rupees (the stock has jumped up to 89.00; I bought this stock yesterday at 82 .. so I made 9% in a day ... ha ). Im putting a buy on Aarvee Denim and Exports Ltd. aswell. The stock is available at 132 rupees (11-Apr), is largely profitable at 37 crs (expected this yr), growing sales and profits and good management.

Bookmark this post: |

|

Wi-fied Pune

A jolly good progressive plan in India " ... a 400 sq km area of Wi-Fi connectivity will enveloping Pune ... " surely raises many an eyebrow. But this seems a reality as the Pune Municipal Corporation and Intel have joined hands to do just that. Here's the link to the article in the Economic Times. Surprisingly, this project would cost the Pune Municipal Corporation a sum of only 7 crores, which means ... Wi-Fi is a truly inexpensive and a quicker option to cables connecting homes to broadband or dial-ups.

Which means ... better infrastructure in Pune, attractive IT destination ... higher property prices. Got that?

Bookmark this post: |

|

Monday, April 10, 2006

Su-Raj diamonds

Su-raj Diamonds should explode at the bourses. Some reasons -

a) The scrip is at a fwdPE of 7.55

b) The NCAV of the stock is a good 97.60 rupees while the CMP is much lower at 64.15 (Apr 7th) - a true Grahamian stock !!!

c) Cash rich company with 26.50 rupees of cash per share

d) Has a dividend yield of almost 2% (which is a rarity these days)

e) The company also has investments of 43.21 crs on it's books

The growth in sales has been good and consistent ... 495 crs (FY02), 583 crs (FY03), 723 crs (FY04) and 1028 crs (FY05). The company would close at 1150 crs for this financial yr ... another rising sales yr. Likewise, growth in profits is at 10.97 crs, 12.11 crs, 21.89 crs and 30.69 crs over the last 4 yrs. I estimate the profits for FY06 to close at 34 crs.

Note, that the P/E ratio of Su-raj Diamonds is much lower than it's peers - Vaibhav Gems, Goldiam International, Rajesh Exports, Shrenuj & Co. etc.

However, Su-raj Diamonds has never moved much. Movement has largely been between the 50 rupees to 70 rupees range over the last one yr. Surprisingly, a number of analysts have given a thums up to the stock over the short and medium term. Here's one by ICICIDirect.

Is this stock worth investing in?

Bookmark this post: |

|

The God of Pennies

I first tracked Hindustan Dorr-Oliver Ltd. in the summer of 2004, somewhere in the month of May. The stock was lingering at around 36 rupees per share. A lot has happened to the stock price and the company over the last 24 months. I am kinda shaken over the current price of the stock, especially when I measure it up with the profit numbers (quarterly data) of the stock ...

Mar-04: 8.78 crs; Jun-04: 0.04 crs; Sep-04: -0.38 crs; Dec-04: -0.91 crs

Mar-05: 2.37 crs; Jun-05: 0.37 crs; Sep-05: 0.39 crs; Dec-05: 2.90 crs

As on 7-Apr-2006, the CMP of the company is at 847.00 rupees. So here is a stock which is at a trailing PE of 154.20 and a fwdPE of 97.90; with an EPS (fwd) of around 9 rupees per share .. and yet commands a market value of 489.52 crores.

Take a bow, gentlemen ... you've just met the god of 'pennies' !!!!

Bookmark this post: |

|

Sunday, April 9, 2006

Munjal Auto

The consistency of growth in sales and profit numbers of Munjal Auto is truly remarkable. The sales / sales growth over LY and profit / profit growth over LY is listed below -

2002 : Sales - 105.63 crs (49.4%); Profit - 11.97 crs (148.0%)

2003 : Sales - 126.61 crs (19.8%); Profit - 13.15 crs (9.80%)

2004: Sales - 159.13 crs (25.68%); Profit - 19.68 crs (49.6%)

2005: Sales - 246.10 crs (54.65%); Profit - 25.98 crs (32.01%)

I estimate the FY2006 numbers on the sales and profit front to close at -

2006: Sales - 375.00 crs (52.37%); Profit - 34.00 crs (30.86%)

Some other important stats about the company -

a) The fwdPE of the scrip is 14.49, which though is not the lowest in it league .. is however among the better one. (I ran a massive filter on some 250+ auto ancillary companies for a minimum of 100 crs sales, profits of atleast 20 crs a year, qtr profits of atleast 6 crs ..... Munjal Auto came a #4 after Pricol, Subros and Amtek India ... I have put the entire list in the comments section)

b) At a dividend of rupees 4.00 for a 10 rupee share, the yield comes to only 1.63%. However, it is estimated that the payout for this yr would gross closer to 5.50 rupees.

c) The NCAV of the scrip is negative 11.52 due to the use of debt, which I feel is never a bad strategy as long as there is enough money to service the debt.

Although Munjal Auto's future is closely linked to that of it's more illustrious customer, Hero Honda Motors Ltd. and to the motorcycle industry per-se - I find the future of the company in good hands. At rupees 245.00, the stock may be a bit higher than the price I might want it at but I am comfortable in looking at a small investment and jacking up if the price diminishes in the short run.

Bookmark this post: |

|

Dial M for ... MRF

It's my opinion that MRF Tyres is overpriced. The scrip touched an all-time high of 3,895.00 rupees on 7th Apr. The charting of the company is enclosed .... (notice the price rise - extreme right)

- Notice the price stabilisation at the 2800-2900 levels (Oct-mid to Jan-end) and once again at the 3100-3200 levels (Feb to Mar). Net net, the price of the stock has vacillated between 2700 and 3250 over the last 7 months.

- The biggest movement post quarter result was when the scrip moved from 2800 to 3230 over 4 days.

- Suprisingly, the scrip has moved from 3050 to 3895 in 6 trading sessions : an increase of 27.7% ... with no supporting news.

- Q1 for the company was marginally better than Q4 of FY2005

At a CMP of 3895.00, MRF is at a fwdPE of 27.76, offers a dividend yield of 0.51%, has a NCAV of only 151.30. The input price (rubber) is on a rising trend - increasing by 50% over the last 12 months (the company is feeling the pinch of the same ... between March and July - historically, rubber prices tend to swell)

It's my opinion that the stock will be range bound ... 3500 to 4000. Which means, there is still money to be made by selling the stock short. An option will need to be considered, however. More on this, if I succeed.

PS: On April 3rd, MRF announced that it'll produce helicopter tyres once it gets the approval. Apparently, Brian Lara was in town for the launch of the same. Surely, that cant be the reason for the huge rise in the stock price.

Bookmark this post: |

|

Tuesday, April 4, 2006

Good advice

1. The recent bull run is a fantastic opportunity for you to sell-off stocks which have not given good profits (and in the future, have a greater probability of not giving you desired returns). So if you haven't done that yet, please use this to it's fullest.

2. Further investment in stocks should always be on the basis of good investment principles. Some ideas -

> Profit for the yr should be no less than 30 crs with a min of 6 crs per quarter

> Exhibit increased sales and profit growth over last three years

> Sales and profit growth for last 4 qtrs vis-a-vis LY quarters

> Price/BV less than 3

> P/E should be less than 66% of industry P/E (mostly fwdP/E < 12)

3. Always see the charting of the stock. www.bseindia.com and www.nseindia.com have the best charting features i've come across. Note, the support and resistance levels over the last one year.

4. Always have a stop loss for any stock you purchase. (and sell when the stop loss is breached; some Buffett-wanabes may think otherwise)

Bookmark this post: |

|

Sunday, April 2, 2006

GNFC Limited

Gujarat Narmada Valley Fertilizers Company Ltd. specs are enclosed -

Share Capital - 146.48 crs

Loans - 299.08 crs

Investment - 218.05 crs

Net CA - 292.47 crs

FV - 10 rupees per share

Dividend - 3.75 rupees per share

CMP - 115.00 rupees per share

LY Profits - 224.20 crs

Examining the balance sheet and the financial statements, I find -

1. The estimated profits for this year would be 270 crs which means a fwdPE of 6.24. Consequently, the sales have been growing at 12% over LY while profits are up, 30% over LY.

2. A dividend yield of 3.16% (on current levels) would only go up this year given the increase in profits. I estimate a dividend payout of 4.5 rupees per share which will propel the dividend yield to 4.11%

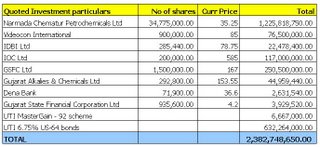

3. The investments shown in the books is at 218 crs. On going through the quoted investments in the balance sheet, I found that the current value of the quoted investments alone comes to 238.27 crs. These are liquid investments and hence can be included in the NCAV also. Here's a review of the quoted investments -

4. NCAV for the scrip (excl investments) is negative 0.05. By including liquid investments (and only 70% of it; I am keeping the remaining 30% as buffer for any plausible reduction in value), then NCAV comes to 14.43 rupees per share.

Finally, news value ... the big news for the company is the merger of the company with it's subsidary, Narmada Chematur Petrochemicals Ltd. The merger proposal was cleared on 2-Mar-2006.

On first count, it seems that this merger is not likely to disturb shareholder value of GNFC. Some reasons are enclosed -

1. NCPL is a profitable company with positive and growing profits QonQ.

2. Amazingly, the current dividend yield and the P/E ratio of this subsidary are better than GNFC (4.26%, 7.21)

3. A consolidated picture would thus be something like -

a) The GNFC share capital would increase by 20.54 crs to 167.02 crs

b) PAT for this year for the combined corporation would close at 300 crs. Thus the fwdPE would be 6.40.

It's a buy from my end with a stop loss at 100 rupees. But also look at NCPL ... seems to be some kind of arbitrage here ...

An arbitrage opportunity :

For every 3 NCPL share, one gets 1 GNFC share. Now GNFC is at 115 rupees and NCPL is at 35 rupees. Which means, if I purchase 3 shares of NCPL at 35 rupees each, my purchase cost would be 105 rupees. And when it gets converted to 1 share of GNFC, the same 105 would be worth 115 rupees. There are many a caveat to this ... but on the face of it, it's almost risk-free.

Bookmark this post: |

|

Micro Inks - a discussion

An interesting discussion on this stock is on at http://valueinvestorindia.blogspot.com. A few premises have been laid -

1. Is the German parent in attempt to delist the company?

2. Or, has something gone terribly wrong - with directors resigning and selling shares?

3. Significance of an open offer of 675 rupees/share to the shareholders of the company on Jan-13-2006. (the steep slide in the share price of the scrip started from then, when it came down from 625 rupees to 410 rupees in the next 30 days)

4. The analyst presentation is rather low on the business strategy of the company. Infact, more stress has been laid on how MHM Holding GmbH can exploit synergies by making India the production base for all it's subsidaries abroad.

... the company has an NCAV of 126 rupees per share which is excellent and a fwdPE of 16.52. Any insights?

Bookmark this post: |

|

The Adventures of Ponty Manesar

Amit has posted a hilarious compilation on the 'Adventures of Ponty Manesar' by Eldo Scaria. The links to the trilogy is enclosed :

1. The Adventures of Ponty Manesar

2. Further Adventures of Ponty Manesar

3. Even more Adventures of Ponty Manesar

The third ODI in Goa, between India and England starts at 9:30 am (IST). Enjoy !!!!

Bookmark this post: |

|

Unichem Labs

The stock jumped by 6.3% today to hit a CMP of 308.00 rupees. Consider exploring this stock for a buy.

Here's why -

a) The stock is available at a fwdPE of 12.36, which is one of the lowest amongst all pharma stocks

b) Although sales are growing slowly, the PAT is zooming at over 20% growth

c) The PAT per quarter has been in upwards of 18 crs over last 3 quarters

d) There is preferential allotment of shares to a private equity firm which has recently jacked up the prices. (the stock grew by 37% in two months)

e) The current dividend yield is 1.14% only. But given the increase in profits this year, I expect an increase in dividend to 5 rupees a share. It wont be more than this as the company is looking at expansion opportunities and acquisitions .. where internal accruals may be more handy than debt.

That apart, I found another swanky news item on Investsmartindia. Diabetes, Cardiology and Anti-infectives are growing areas in the healthcare segment. Buy in low numbers now and increase stake if it drops anywhere.

Bookmark this post: |

|

Saturday, April 1, 2006

It aint done till, it's done

The picture above is what provisionally sixth placed Giancarlo Fisichella saw, as P5 Jenson Button's engine blew at the penultimate turn of the Australian GP. Inspite of a blown engine, Button didn't remove the foot from the pedal in a serious bid to cross the line ... he finished a menacing 7 metres from the finish line. Ironically, Jenson Button started on pole position at the start of the race. News

Well (sob, sob ...) this is the second time, I've lost a bet because of engine blowups in the last lap of a race. The last occasion was when Mika Hakkinen's splendid drive around the 2001 Spanish circuit came to a close as his Mercedes engine gave way to a lucky Michael Schumacher.

Bookmark this post: |

|